Report ID: 1017 |

Published Date: 16 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Surgical Imaging Market Outlook:

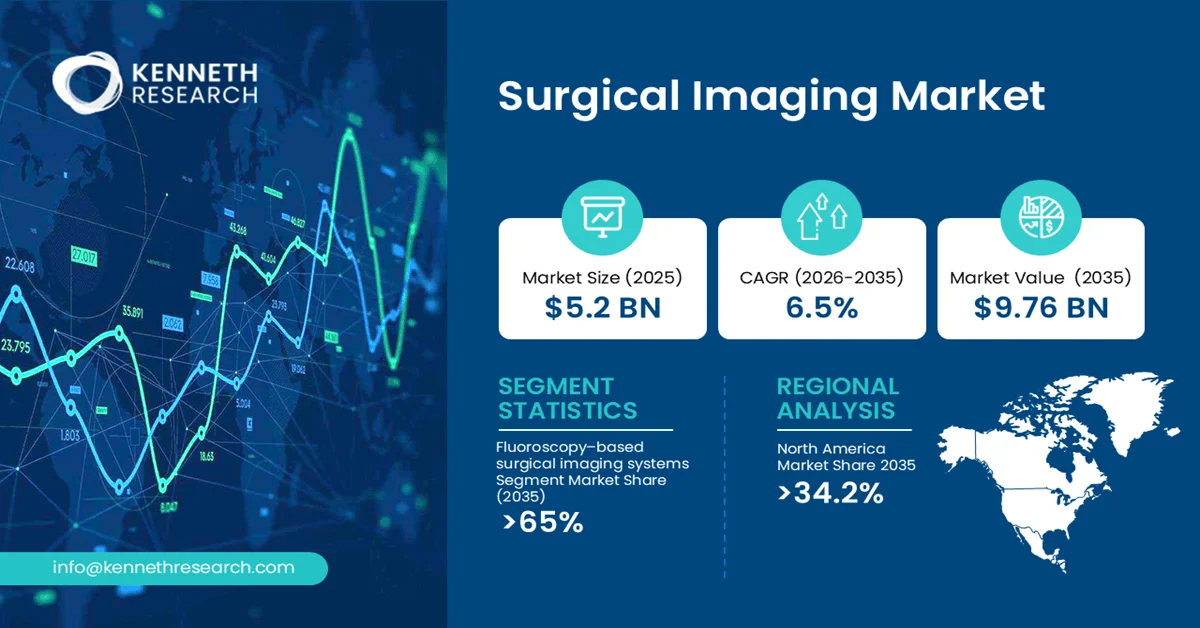

The global surgical imaging market size reached USD 5.2 billion in 2025 and is projected to value at USD 9.76 billion by the end of 2035, expanding at a CAGR of 6.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of surgical imaging is estimated at USD 5.54 billion.

Adoption of surgical imaging technologies is accelerating globally, driven by the rising volume of surgical procedures and the proliferation of hybrid operating rooms that integrate advanced imaging capabilities directly into surgical environments. The shift toward minimally invasive techniques demands high-resolution, real-time visualization that traditional open surgery does not require. Technological convergence—where systems now combine 2D/3D imaging, fluorescence guidance, and navigation into unified platforms—further propels market expansion.

The surgical imaging market encompasses advanced medical visualization technologies deployed in operating rooms to provide real-time anatomical guidance during invasive procedures. This market includes imaging modalities such as fluoroscopy, computed tomography (CT), magnetic resonance imaging (MRI), ultrasound, and C-arm systems, which enable surgeons to navigate complex anatomical structures with enhanced precision. These systems serve as the visual backbone of modern operating theaters, facilitating intraoperative decision-making across orthopedics, neurosurgery, cardiovascular interventions, and trauma surgery.

Key Surgical Imaging Market Insights Summary:

Key Takeaways: Market Trends & Insights

- The global surgical imaging market size reached USD 5.2 billion in 2025

- The market is projected to reach USD 9.76 billion by the end of 2035

- The market is expected to expand at a CAGR of 6.5% during the forecast period (2026–2035)

In 2026, the industry size is estimated at USD 5.54 billion - The Fluoroscopy–based surgical imaging systems segment dominated with a 65% share in 2025

- North America led the global market, accounting for 34.2% of the share in 2025

- Key drivers include rising surgical procedure volumes and technological advancements in imaging modalities

- Major players include GE HealthCare, Siemens Healthineers AG, and Koninklijke Philips N.V.

- U.S. CAGR (2026–2034): 6.4%

- Japan CAGR (2026–2034): 6.0%

Market Drivers

- Rising Surgical Procedure Volumes Worldwide

- Technological Advancements in Surgical Imaging Modalities

- Expansion of Ambulatory Surgical Centers (ASCs)

- Prevalence of Chronic Diseases Requiring Surgical Intervention

Challenges

- High Capital Expenditure and Procurement Barriers

- Stringent Regulatory Approval Pathways and Clinical Validation Requirements

Surgical Imaging Market Overview & Supply Chain

Technological convergence, where modern platforms now integrate 2D/3D imaging, fluorescence guidance, and artificial intelligence-driven analytics into unified systems, represents a paradigm shift in surgical workflow optimization. Technological advancement, coupled with procedural growth trajectory, directly reinforces the critical need for advanced surgical imaging infrastructure across healthcare systems worldwide, with implications extending through the forecast period as surgical backlogs are addressed and procedure complexity escalates.

The surgical imaging value chain begins with raw material and component inputs, encompassing specialized X-ray tubes, flat-panel detectors, high-grade semiconductors, CMOS sensors, and medical-grade metals and polymers. These components are sourced from a concentrated network of specialized suppliers, often requiring stringent regulatory certifications for biocompatibility, radiation shielding, and electromagnetic interference compliance.

The manufacturing phase involves precision assembly and system integration, where OEMs combine hardware components with proprietary imaging software, image-processing algorithms, and user-interface platforms. Production occurs in highly regulated facilities adhering to ISO 13485 and FDA Quality System Regulations, with rigorous calibration and quality assurance protocols to ensure imaging fidelity and radiation safety standards.

Distribution channels operate through a hybrid model: direct sales forces for large hospital networks and group purchasing organizations, supplemented by specialized medical distributors for regional healthcare facilities and ambulatory surgical centers. Value-added resellers often provide installation, training, and maintenance services, creating recurring revenue streams.

Surgical Imaging Market: Growth Drivers & Challenges

Growth Drivers:

- Rising Surgical Procedure Volumes Worldwide: The global escalation in surgical interventions serves as a primary catalyst for surgical imaging adoption. As healthcare access expands and aging populations require more procedures, the volume of surgeries has surged significantly, directly increasing demand for intraoperative imaging technologies that enable precision and safety. This procedural growth translates to sustained demand for surgical imaging systems across orthopedic, cardiovascular, and trauma applications. According to the Government of Saskatchewan, the number of surgeries performed in fiscal year 2023-24 surpassed the previous record set in 2022-23 by nearly 6,000 procedures, with a total of 95,700 surgeries completed—the highest annual surgical volume ever documented in the province. Notably, hip and knee replacement volumes rose from approximately 6,300 to nearly 7,100 annually, representing a 50% increase over pre-pandemic levels recorded in 2019-20. This procedural growth trajectory has direct implications extending through 2035 as healthcare systems worldwide invest in imaging infrastructure to manage mounting surgical backlogs and rising procedure complexity.

- Technological Advancements in Surgical Imaging Modalities: Over the past decade, the surgical imaging industry has experienced a major transformation driven by innovations in imaging technology. Modern systems provide faster operation, higher image quality, and simpler interfaces compared to traditional systems. In 2024, GE HealthCare introduced the OEC 3D, a mobile C-arm with 2D and 3D cone-beam CT imaging using CMOS flat panel technology, capable of acquiring high-resolution 3D volumes within 30 seconds for intraprocedural use in endovascular, orthopedic, and spine procedures. Siemens Healthineers launched the CIARTIC Move in March 2024, a self-driving mobile 3D C-arm with automated workflows and effortless handling for intraoperative 2D and 3D imaging. The latest devices integrate multiple modalities—2D/3D imaging, fluorescence, and navigation—into unified systems that reduce OR space requirements and streamline image management. This convergence creates powerful network effects, with hospital procurement decisions increasingly favoring comprehensive platforms over standalone devices. This trend will likely accelerate through the forecast period, making hybrid operating rooms the standard for complex surgical procedures across North America and Asia Pacific markets.

Challenges:

- High Capital Expenditure and Procurement Barriers: Surgical imaging systems—particularly advanced modalities such as intraoperative CT, hybrid imaging platforms, and robotic-assisted navigation systems—require substantial upfront capital investment, often ranging from USD 200,000 to over USD 1 million per unit. This financial burden is compounded by additional costs for installation, shielding infrastructure, specialized operating room modifications, and ongoing maintenance contracts. Smaller hospitals, ambulatory surgical centers with limited budgets, and healthcare facilities in emerging economies face significant procurement barriers.

- Stringent Regulatory Approval Pathways and Clinical Validation Requirements: Surgical imaging systems are classified as Class II or Class III medical devices by regulators such as the U.S. Food and Drug Administration and comparable agencies worldwide. Market clearance requires extensive clinical evidence demonstrating safety, imaging efficacy, and equivalence or superiority to predicate devices. The 510(k) and Pre-Market Approval processes involve rigorous testing, clinical trial data, and quality system audits, often spanning 12–36 months from submission to clearance. Extended regulatory timelines delay product launches, increase development costs, and create competitive disadvantages for smaller innovators lacking dedicated regulatory affairs teams.

Surgical Imaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

6.5% |

| Base Year Market Size (2025) |

USD 5.2 billion |

| Forecast Year Market Size (2035) |

USD 9.76 billion |

| Regional Scope |

|

Surgical Imaging Market Segmentation Analysis:

Product Type Segment Analysis

Fluoroscopy–based surgical imaging systems dominate the surgical imaging market, accounting for 65% segment share in 2025.

The segment growth is driven by their unparalleled ability to deliver real-time, high-resolution visualization during complex surgical procedures. These systems, particularly mobile C-arms equipped with image intensifier technology, provide continuous X-ray imaging that enables surgeons to monitor instrument positioning, implant placement, and anatomical changes instantaneously. Supply-side factors also bolster the segment's dominance. Original equipment manufacturers continue to invest in next-generation fluoroscopy platforms featuring automated positioning, low-dose radiation protocols, and AI-enhanced image processing. Government healthcare data from England substantiates this demand: in 2021/22, 916,335 fluoroscopy procedures were performed across NHS facilities, reflecting recovery from pandemic-related disruptions. The future outlook remains positive through 2035, as aging populations drive orthopedic and cardiovascular procedure volumes, sustaining fluoroscopy's position as the cornerstone of intraoperative imaging.

Technology Segment Analysis

Within the technology segmentation, 2D imaging systems are projected to maintain a dominant market share through the forecast period, underpinned by their widespread installed base, cost-effectiveness, and clinical versatility.

Current demand drivers center on the critical need for reliable, high-resolution, and cost-effective imaging for routine surgical guidance across high-volume specialities such as orthopedics, trauma, and general surgery. Industry adoption trends indicate a continued preference for 2D systems in mid-sized and smaller healthcare facilities and emerging markets where budget constraints are a significant factor. While 3D and AI-enabled systems are advancing rapidly, 2D fluoroscopy C-arms—particularly portable units—remain the workhorse for intraoperative guidance due to their ease of use and immediate integration into existing OR workflows.

Our in-depth analysis of the global surgical imaging market includes the following segments:

|

Segments |

Sub-Segments |

|

Product Type |

|

|

Technology |

|

|

Application |

|

|

End-user |

|

Surgical Imaging Market Regional Insights:

North America Market Trends & Insights:

North America leads the global surgical imaging market, accounting for 34.2% of the market share in 2025. This dominance is anchored in the region's advanced healthcare infrastructure, characterized by widespread adoption of next-generation intraoperative imaging technologies and strong integration of AI-powered visualization and data management systems. Production and consumption are reinforced by the strong presence of major medical technology companies headquartered in the U.S., ensuring a continuous pipeline of innovation and supply. Investment is robust, fueled by the rapid expansion of hybrid operating rooms equipped with real-time imaging capabilities, along with favorable reimbursement policies that encourage adoption of new surgical technologies. Regulatory support from bodies like the FDA, with its 510(k) clearance pathway, facilitates the swift commercialization of advanced systems. This regulatory and investment climate cements North America's dominant position in the global market.

Within the region, the United States serves as the primary growth engine, and is driven by the high volume of complex surgical procedures, a significant shift toward minimally invasive procedures, and substantial R&D investments by leading firms. The high demand for surgical procedures is illustrated by data from the Agency for Healthcare Research and Quality (AHRQ), which recorded over 9 million ambulatory surgery encounters in its 2022 Nationwide Ambulatory Surgery Sample.

The Canada surgical imaging market is propelled by robust healthcare spending, a growing adoption of image-guided and robot-assisted surgical systems, and infrastructure investments aimed at managing rising surgical volumes. This high procedure volume ensures North America's continued dominance through the forecast period.

Asia Pacific Market Trends & Insights:

Asia Pacific represents the secondary region in the global surgical imaging market, following North America's dominant position. Market demand across the region is propelled by rapidly expanding healthcare infrastructure, rising medical tourism, and a growing burden of chronic diseases requiring surgical intervention. Industrial activity is concentrated in established manufacturing hubs—Japan and China—where major OEMs operate production facilities for surgical imaging systems, while emerging economies such as India and Southeast Asian nations are witnessing a surge in healthcare facility construction and medical equipment procurement.

In China, the market benefits from the government's Made in China 2025 initiative, which promotes domestic manufacturing of high-end medical devices, including surgical imaging systems. The country's vast hospital network and increasing procedure volumes—particularly in trauma and orthopedics—sustain robust demand for C-arms and intraoperative CT systems. Additionally, the government's tiered healthcare system reform is driving equipment procurement at county-level hospitals, creating significant opportunities for mid-tier imaging systems.

Japan surgical imaging market represents a mature yet dynamic landscape, characterized by high technology adoption rates, an aging demographic profile, and a well-established reimbursement framework for advanced surgical procedures. The country's emphasis on robotics-assisted surgery and precision medicine creates sustained demand for integrated imaging platforms that complement robotic surgical systems, ensuring continued market expansion through the forecast period.

Leading Companies Operating in the Global Surgical Imaging Market:

The surgical imaging market is consolidated, with GE HealthCare, Siemens Healthineers AG, and Koninklijke Philips N.V. accounting for a significant global market share due to their comprehensive product portfolios, technological innovation, and extensive geographic presence. These leaders compete through continuous product launches integrating AI-driven image analysis, augmented reality navigation, and advanced 3D imaging capabilities. The competitive landscape is characterized by vertical integration across imaging hardware, software, and navigation platforms, with OEMs investing in strategic partnerships and acquisitions to expand their surgical imaging ecosystems. Regional players such as Shimadzu, Ziehm Imaging, and Hologic maintain significant positions through specialization in specific modalities or strong regional distribution networks.

Here is a list of key players operating in the global surgical imaging market:

|

Company |

Specialty |

HQ |

Position |

|

GE HealthCare |

AI-enabled C-arms and surgical navigation systems |

USA |

Leader |

|

Siemens Healthineers AG |

Mobile C-arms, fluoroscopy, and hybrid OR imaging systems |

Germany |

Leader |

|

Koninklijke Philips N.V. |

Hybrid OR solutions and image-guided therapy systems |

Netherlands |

Leader |

|

Shimadzu Corporation |

Mobile C-arms and fluoroscopic imaging systems |

Japan |

Major |

|

Ziehm Imaging GmbH |

Mobile C-arm technology for orthopedic and endovascular procedures |

Germany |

Major |

|

Hologic, Inc. |

Mini C-arms for orthopedic and extremity imaging |

USA |

Major |

|

Stryker |

Intraoperative imaging integrated with surgical navigation platforms |

USA |

Major |

|

Canon Medical Systems Corporation |

Intraoperative CT and fluoroscopy systems |

Japan |

Major |

|

Medtronic |

Imaging systems integrated with surgical navigation for neurosurgery and spine |

Ireland |

Major |

Recent Developments

- In July 2025, the U.S. Food and Drug Administration granted 510(k) clearance (K251523) for the Siemens Healthineers' Cios Spin mobile X-ray system. This clearance expands Siemens Healthineers' mobile C-arm portfolio with enhanced software features—including updated Retina 3D for enlarged 3D volumes, NaviLink 3D Lite, and a Universal Navigation Interface—reinforcing the company's competitive position in the intraoperative imaging segment.

- In April 2025, the FDA posted a Class 2 recall for Philips' Zenition 70 mobile C-arm systems, following the company's February 2025 initiation of corrective action. The recall was prompted by a defect in the wireless foot switch pedal that may get stuck in the active position, resulting in unintended radiation emission. This quality event represents a competitive setback for Philips in the mobile C-arm segment, potentially impacting customer confidence and creating opportunities for competitors to capture share while Philips implements corrective actions, including IFU addendums and on-site inspections.

Frequently Asked Question

In 2026, the surgical imaging market exceeded USD 5.54 billion.

The surgical imaging market is projected to reach USD 9.76 billion by the end of 2035, expanding at a CAGR of 6.5% over the forecast period (2026–2035).

The major players in the market are GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., Shimadzu Corporation, Ziehm Imaging GmbH, Hologic, Inc., Stryker, Canon Medical Systems Corporation, Medtronic, and others.

In the Product Type segment, the Fluoroscopy–based surgical imaging systems sub-segment is anticipated to capture the largest market share of 65% in the future and exhibit lucrative growth opportunities during 2026–2035. This growth trajectory is largely attributed to rising surgical procedure volumes worldwide, which drive sustained demand for real-time intraoperative imaging guidance.

North America is projected to hold the largest market share of 34.2% by the end of 2035 and provide more business opportunities in the future. Continuous investments in hybrid operating room infrastructure and strong regulatory support through FDA clearance pathways are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1017 |

Published Date: 16 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy