Report ID: 1011 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Solid State Battery Market Outlook:

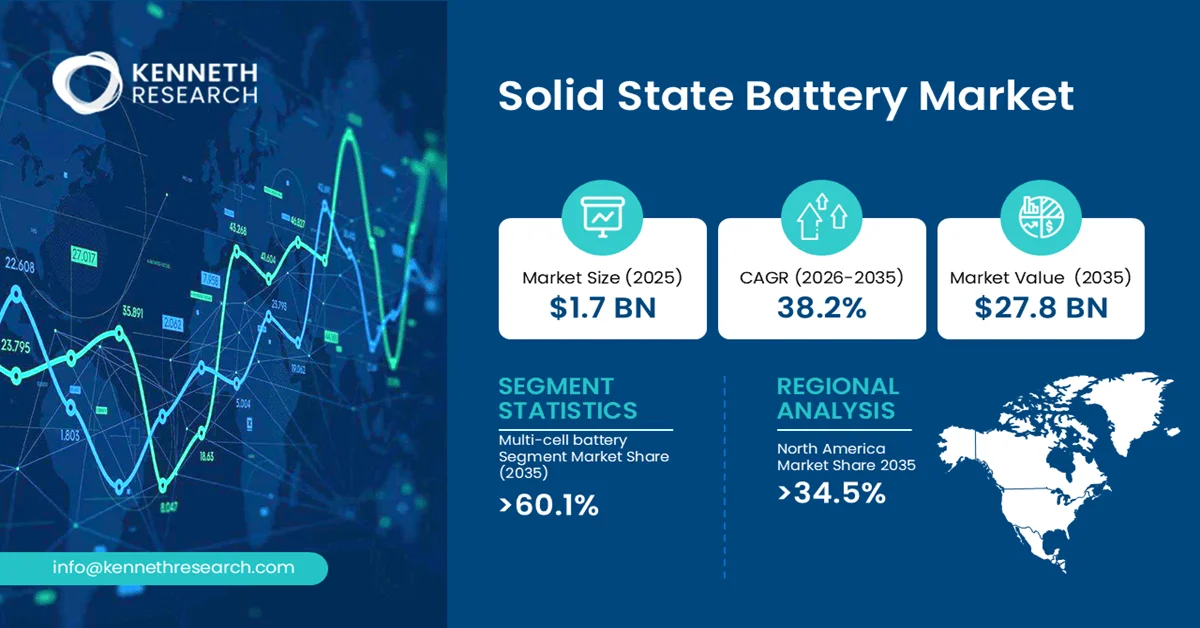

The global solid state battery market size was valued at USD 1.7 billion in 2025 and is projected to reach USD 2.4 billion in 2026. In addition, the solid state battery industry is further expected to be worth USD 27.8 billion by the end of 2035, rising at a CAGR of 38.2% during the forecast period, i.e., 2026-2035.

Accelerating demand for higher energy density and safety over conventional lithium-ion batteries, driven by electric vehicle (EV) range anxiety and fire-safety regulations. Government mandates for EV adoption and stationary storage reliability are forcing OEMs to transition from liquid-electrolyte to solid-state architectures.

Solid state batteries are advanced energy storage devices that replace the liquid or gel electrolyte used in conventional lithium-ion batteries with a solid electrolyte. This design improves battery safety, energy density, thermal stability, and operational lifespan while reducing the risk of leakage and thermal runaway. The automotive sector is particularly driving research and commercialization efforts because solid state batteries offer the potential for longer driving ranges and faster charging times compared to conventional battery technologies. According to the International Energy Agency, battery demand in the energy sector surpassed 1 TWh in 2024, driven largely by electric vehicle adoption, highlighting the need for advanced battery technologies capable of supporting future energy and mobility requirements.

Key Solid State Battery Market Insights Summary:

Key Takeaways: Market Trends & Insights

- In the category segment, the multi-cell battery sub-segment is anticipated to capture the revenue share of 60.1% during 2026-2035

- North America solid state battery market is projected to hold the largest revenue share of 34.5% by the end of 2035

- The U.S. alone accounts for over 74.6% of the North America market in 2026

- Japan held an estimated 15.7% share of the global solid state battery market in 2025

- The major players in the market are Toyota, Panasonic, Samsung SDI, CATL, BYD, and others.

Market Drivers

- Rapid expansion of electric vehicle electrification

- Increasing demand for high-performance consumer electronics

- Rising investment in advanced battery research and commercialization

- Manufacturing Cost Reduction Breakthroughs in Solid Electrolytes

Challenges

- High manufacturing complexity and production costs

- Material performance and long-term reliability limitations

Solid State Battery Market Overview & Supply Chain

The solid state battery industry value chain begins with the sourcing of critical raw materials, including lithium, nickel, cobalt, manganese, graphite, ceramic electrolytes, sulfide compounds, and advanced polymer materials. Demand for these minerals continues to rise alongside battery deployment; according to the International Energy Agency (IEA), lithium demand increased by approximately 30% in 2023, while demand for nickel, cobalt, and graphite expanded by 8-10%, highlighting the growing importance of upstream supply security.

Key end users include electric vehicle manufacturers, consumer electronics companies, aerospace organizations, industrial equipment suppliers, and energy storage system developers. Major stakeholders across the value chain comprise mining companies, material refiners, battery manufacturers, technology developers, research institutions, OEMs, government agencies, and recycling firms that support circular battery material recovery. Demand for EV batteries exceeded 750 GWh in 2023, reinforcing the strategic importance of resilient battery supply chains.

Solid State Battery Market: Growth Drivers & Challenges

Growth Drivers:

- Manufacturing Cost Reduction Breakthroughs in Solid Electrolytes: Historically, prohibitive manufacturing costs, particularly high-temperature sintering and expensive mother powder waste, have delayed commercial scale-up. However, recent innovations in oxide-based electrolyte processing have reduced production costs by over 90%. The Korea Research Institute of Standards and Science (KRISS) developed a Li-Al-O multifunctional coating that eliminates expensive mother powder while achieving record electrolyte density exceeding 98.2% and ionic conductivity more than double conventional materials. Large-area solid electrolyte membranes (16 cm²) are now feasible with 99.9% yield, compared to laboratory-scale pellets that previously cost over USD 550 per 1 cm diameter unit. This breakthrough enables domestic production in markets like South Korea and can be replicated across Japan and India under technology transfer agreements.

- Rapid Expansion of Electric Vehicle Electrification: The accelerating adoption of electric vehicles (EVs) is a major growth driver for the solid state battery market. Automakers are seeking battery technologies capable of delivering higher energy density, improved safety, shorter charging times, and longer driving ranges than conventional lithium-ion batteries. Solid-state batteries address these requirements by utilizing solid electrolytes that reduce fire risks and support advanced electrode architectures. According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, accounting for more than 20% of new vehicle sales worldwide. This growing EV fleet is expected to accelerate the commercialization of next-generation battery technologies over the coming decade.

Challenges:

- High Manufacturing Complexity and Production Costs: One of the most significant restraints facing the solid state battery market is the complexity associated with large-scale manufacturing. Unlike conventional lithium-ion batteries, solid-state designs require highly specialized materials, precision engineering, and advanced fabrication processes to ensure stable interfaces between solid electrolytes and electrodes. Maintaining consistent performance across large production volumes remains technically challenging, resulting in lower manufacturing yields and higher production costs. The industry impact is particularly evident during the transition from pilot-scale production to commercial-scale manufacturing, where companies must invest heavily in specialized equipment, process optimization, and quality control systems.

- Material Performance and Long-Term Reliability Limitations: Another major restraint is the difficulty of achieving consistent long-term performance under real-world operating conditions. Solid-state batteries rely on complex interactions between solid electrolytes, cathodes, and anodes, and performance degradation can occur due to interface instability, mechanical stress, dendrite formation, and reduced ionic conductivity over extended usage cycles. These technical limitations create uncertainty for industries that require highly reliable energy storage solutions, particularly automotive, aerospace, and industrial applications. From a commercial perspective, concerns regarding durability, lifecycle performance, and warranty liabilities can slow technology adoption and increase qualification timelines.

Solid State Battery Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

38.2% |

| Base Year Market Size (2025) |

USD 1.7 billion |

| Forecast Year Market Size (2035) |

USD 27.8 billion |

| Regional Scope |

|

Solid State Battery Market Segmentation Analysis:

Category Segment Analysis

The multi-cell battery sub-segment in the category segment is anticipated to garner the largest share of 60.1% by the end of 2035.

The multi-cell battery sub-segment dominates the solid state battery market, driven by unparalleled energy density and safety advantages over single-cell configurations. Multi-cell architectures, comprising multiple solid-state cells stacked in series or parallel, enabling higher voltage output and scalable capacity, making them indispensable for electric vehicle (EV) powertrains and grid-scale storage systems. Automotive OEMs prioritize multi-cell packs to achieve 500+ km driving ranges while eliminating thermal runaway risks inherent to conventional lithium-ion batteries. The U.S. Department of Energy (DOE) has identified multi-cell solid-state manufacturing as a critical national priority. Major automakers including Toyota, BMW, and Nissan have accelerated multi-cell battery validation programs. In April 2023, the DOE issued a $16 million lab call specifically targeting large format or high-volume manufacturing of solid state batteries.

Application Segment Analysis

The consumer electronics sub-segment in the application segment is projected to hold a considerable share during the forecast period.

The consumer electronics sub-segment is experiencing significant growth due to increasing demand for compact, lightweight, and high-performance energy storage solutions. Manufacturers of smartphones, laptops, wearable devices, tablets, and emerging smart devices are seeking batteries that provide longer operating life, enhanced safety, and faster charging capabilities. According to the International Telecommunication Union (ITU), approximately 5.5 billion people were using the Internet in 2024, representing about 68% of the global population. The expanding digital ecosystem continues to drive demand for connected consumer devices, creating long-term opportunities for advanced battery technologies.

Our in-depth analysis of the global solid state battery market includes the following segments:

|

Segment |

Sub-segment |

|

Category |

|

|

Application |

|

|

Type |

|

|

Capacity |

|

Solid State Battery Market Regional Insights:

North America Market Trends & Insights:

North America is expected to maintain its leadership position by grabbing the highest share of 34.5% in the solid state battery market.

The market upliftment is primarily attributed to strong investments in battery innovation, advanced manufacturing capabilities, supportive policy frameworks, and a well-established electric vehicle ecosystem. The region benefits from extensive research and development activities led by battery developers, automotive manufacturers, national laboratories, and academic institutions. Public and private sector investments are accelerating the commercialization of next-generation battery technologies, including solid-state batteries, to strengthen domestic energy storage and transportation supply chains. According to the International Energy Agency (IEA), electric car sales in the United States reached approximately 1.6 million units in 2024, reinforcing the region's position as a major market for advanced battery technologies.

The U.S. drives this regional dominance through coordinated policy action. The U.S. Department of Energy (DOE) has issued multiple funding initiatives targeting manufacturing scale-up, including collaborations between national laboratories and industry partners to transition solid-state electrolyte research into large-format, high-volume production. In September 2024, Solid Power secured up to $50 million in DOE funding to enhance sulfide-based solid electrolyte production, with the company contributing in matching funds under a cost-sharing arrangement. The DOE has characterized solid-state lithium batteries as providing an energy-dense and safer alternative to lithium-ion batteries currently used for electric vehicles.

Canada complements the region’s manufacturing leadership through critical mineral supply chain integration. As a reliable trading partner under the U.S.-Canada Critical Minerals Action Plan, Canada supplies high-purity lithium, graphite, and rare earth elements essential for solid-state electrolyte production. The country’s government incentives for battery innovation, including the Strategic Innovation Fund and critical mineral exploration tax credits, position the country as an upstream materials hub feeding U.S. gigafactories. By 2035, with integrated regional production, the U.S. cell assembly paired with Canada-based mineral processing is poised to uplift the market.

Asia Pacific Market Trends & Insights:

The Asia Pacific represents the fastest-growing region for the solid state battery market.

The growth in the region is driven by concentrated original equipment manufacturer (OEM) activity and aggressive national technology roadmaps. The demand is anchored by electric vehicle (EV) production, especially with China-based manufactures over 60% of global EVs, creating immediate off-take opportunities for solid-state battery integration. Industrial activity spans the full value chain: Japan leads in electrolyte materials research and precision manufacturing, while India is emerging as a cost-competitive assembly destination. Future opportunities lie in cross-border joint ventures between Japan-based material suppliers and China-specific pack assemblers, enabling a suitable partnership for market expansion.

Japan serves as the technology epicenter of regional solid-state battery ecosystem. Toyota, Panasonic, and Hitachi Zosen operate the region's most advanced pilot lines, with Toyota’s next-generation BEV battery development and production plan successfully certified by METI in September 2024. Japan's strength lies in sulfide-based solid electrolytes, where its precision ceramics industry provides a transferable manufacturing advantage. Government-backed consortia (LIBTEC) coordinate pre-competitive research, reducing duplication across automakers and battery divisions.

China is the volume leader and cost competitor. Contemporary Amperex Technology Co., Limited (CATL) have announced a surge in lithium-ion battery sales to 661 GWh, denoting an increase by 39%. China's advantage includes state-backed critical mineral control and aggressive provincial subsidies for dry-room infrastructure. Therefore, the country is poised to lead in low-to-mid energy density solid-state cells for commercial EVs, while Japan retains premium automotive and specialty electronics segments.

Leading Companies Operating in the Global Solid State Battery Market:

The competitive landscape of the solid state battery market is characterized by a mix of established automotive-electronic conglomerates, specialized battery pure-plays, and state-backed national champions. Traditional lithium-ion giants are pivoting to solid-state through internal R&D and strategic partnerships, while specialized firms leverage patented electrolyte chemistries to secure automotive tier-1 relationships. Consolidation is accelerating via SPAC mergers and government co-investment programs. Regional concentration remains high, with Japan housing the deepest patent portfolios, China leading in manufacturing scale, and North America advancing through DOE-funded pilot lines.

Here is a list of key players operating in the global solid state battery market:

|

Company |

Specialty |

HQ |

Position |

|

Toyota |

Sulfide-based solid-state for automotive EVs |

Japan |

Leader |

|

Panasonic |

Ceramic electrolyte cells for consumer and automotive |

Japan |

Leader |

|

Samsung SDI |

Oxide-solid battery for wearables and EVs |

South Korea |

Leader |

|

CATL |

Condensed-state and semi-solid battery scale manufacturing |

China |

Leader |

|

BYD |

Integrated solid-state pack design for commercial EVs |

China |

Major |

|

Solid Power |

Sulfide electrolyte production and licensing |

USA |

Major |

|

Factorial Inc. |

Quasi-solid-state polymer-electrolyte for premium EVs |

USA |

Major |

|

ProLogium |

Inorganic superfluidized solid-state for multiple applications |

Taiwan |

Major |

|

Hitachi Zosen |

Ceramic solid-state for industrial and medical |

Japan |

Niche |

|

WeLion New Energy |

Semi-solid and solid-state for EVs and energy storage |

China |

Niche |

Recent Developments

- In May 2026, ProLogium Holding Inc. and Translational Development Acquisition Corp. entered into a definitive deal for a business combination that is predicted to lead in ProLogium becoming a publicly listed company and escalated the commercialization of industry-leading solid state batteries.

- In December 2025, Factorial Inc. and Cartesian Growth Corporation III effectively entered into a definitive business combination agreement for valuing Factorial at an estimated %1.1 billion on a pre-merger and pre-money basis, along with the inclusion of %100 million in newest capital committed by institutional investors.

- In March 2025, BASF, Yangtze River Delta Physics Research Center Co., Ltd., and Beijing WELION New Energy Technology Co., Ltd. significantly signed a groundbreaking cooperation agreement and developed the next-generation solid-state battery pack, incorporating non-metallic components designed with advanced material solutions to enhance lightweighting, thermal safety management, and functionality.

Frequently Asked Question

In 2025, the solid state battery market exceeded USD 1.7 billion.

The solid state battery market is projected to reach USD 27.8 billion by the end of 2035, expanding at a CAGR of 38.2% over the forecast period (2026-2035).

The major players in the market are Toyota Motor Corporation, QuantumScape Corporation, PowerCo, BASF SE, WELION New Energy Technology Co., Ltd., IOPLY, and others.

In the category segment, the multi-cell battery sub-segment is anticipated to capture the largest market share of 60.1% in the future and exhibit lucrative growth opportunities during 2026-2035. This growth trajectory is largely attributed to increasing demand for high-capacity battery systems in electric vehicles, industrial equipment, and advanced energy storage applications.

North America is projected to hold the largest market share of 34.5% by the end of 2035 and provide more business opportunities in the future. Continuous investments in battery innovation, electric vehicle manufacturing, and advanced energy storage technologies across the U.S. and Canada are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1011 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy