Report ID: 1009 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Solar Panel Recycling Market Outlook:

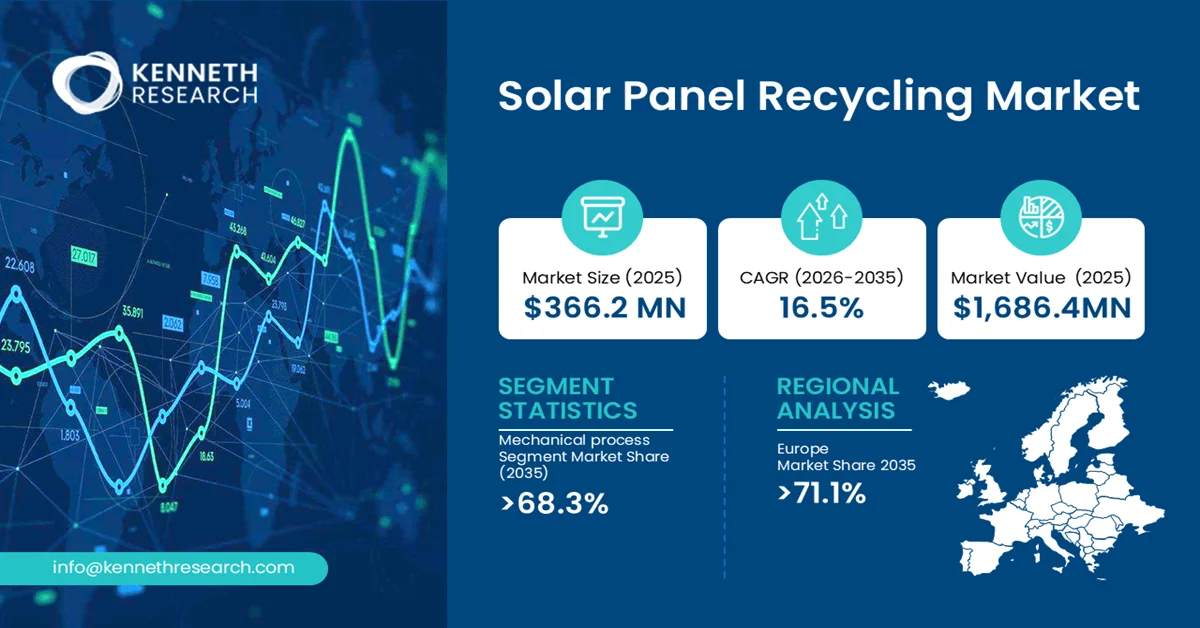

The global solar panel recycling market size was valued at USD 366.2 million in 2025 and is projected to reach USD 426.6 million in 2026. In addition, the solar panel recycling industry is further expected to be worth USD 1,686.4 million by the end of 2035, rising at a CAGR of 16.5% during the forecast period, i.e., 2026-2035.

The primary growth driver of the Solar Panel Recycling Market is the rapid increase in end-of-life photovoltaic (PV) modules generated from early solar installations, combined with tightening global regulations mandating sustainable waste management and recovery of valuable materials such as silicon, silver, aluminum, and glass through circular economy frameworks.

The solar panel recycling market refers to the industrial ecosystem involved in the collection, dismantling, processing, and recovery of valuable materials from end-of-life solar photovoltaic (PV) modules. This market includes mechanical, thermal, and advanced separation technologies designed to extract reusable components such as silicon wafers, aluminum frames, glass sheets, and precious metals like silver. It plays a critical role in supporting the renewable energy lifecycle by ensuring that solar installations remain environmentally sustainable beyond their operational lifespan.

Key Solar Panel Recycling Market Insights Summary:

Key Takeaways: Market Trends & Insights

- In the process segment, the mechanical process sub-segment is anticipated to capture the revenue share of 68.3% during 2026-2035

- Europe solar panel recycling market is projected to hold the largest revenue share of 71.1% by the end of 2035

- The solar panel recycling market in the U.S. garners 9.2% of the global market share

- The major players in the market are Solarcycle, SoliTek, Rinovasol, Veolia, and others.

Market Drivers

- Expansion of global solar PV installations leading to higher future end-of-life module volumes

- Rising demand for critical raw materials such as silicon, silver, and aluminum through recycling

- Corporate ESG commitments driving adoption of circular economy and sustainable sourcing models

- Increasing investments in dedicated solar waste collection and reverse logistics infrastructure

Challenges

- Supply Chain Complexity and Dependence on Specialized Semiconductor Materials

- High Qualification Requirements and Extended Product Commercialization Cycles

Solar Panel Recycling Market Overview & Supply Chain

The solar panel recycling market value chain begins with end-of-life photovoltaic (PV) modules, sourced primarily from utility-scale solar farms, commercial rooftop installations, and residential solar systems reaching decommissioning. These discarded panels are collected through reverse logistics networks operated by waste management companies, solar EPC contractors, and producer responsibility organizations. At the processing stage, recycling firms dismantle modules and separate core materials through mechanical, thermal, or advanced chemical techniques. Recovered outputs include aluminum frames, glass sheets, silicon wafers, copper wiring, and trace precious metals, which are then refined and upgraded for reuse in industrial manufacturing.

Distribution channels connect recyclers with downstream industries such as solar panel manufacturers, electronics producers, and raw material suppliers who reintegrate recovered inputs into production cycles. End users primarily include photovoltaic manufacturers and construction material industries focused on sustainable sourcing. Key stakeholders span OEM solar manufacturers, recycling technology providers, utility operators, government regulators, and circular economy compliance bodies, collectively shaping a regulated and increasingly integrated circular supply ecosystem.

Solar Panel Recycling Market: Growth Drivers & Challenges

Growth Drivers:

- Strengthening Regulatory Mandates for Circular Solar Waste Management: The solar panel recycling market is primarily driven by increasingly stringent regulatory frameworks governing electronic and photovoltaic waste management. Governments are enforcing extended producer responsibility (EPR) models that require manufacturers and importers to manage end-of-life solar modules, ensuring systematic collection and material recovery rather than landfill disposal. The European Union’s Waste Electrical and Electronic Equipment (WEEE) Directive mandates a 65% collection target for electronic waste, including photovoltaic modules, reinforcing structured recycling adoption across member states. This regulatory push is accelerating the establishment of formal recycling infrastructure across major solar-adopting regions, particularly Europe and North America.

- Advancements in High-Efficiency Material Recovery Technologies: Technological advancements in recycling processes are significantly enhancing the economic viability of solar panel recycling. Innovations in mechanical separation, thermal delamination, and emerging chemical recovery techniques are improving the extraction efficiency of high-value materials such as silicon, silver, aluminum, and copper. These improvements are reducing processing losses and increasing the purity levels of recovered outputs, making recycled materials more competitive with virgin raw materials. Looking ahead, continued R&D investment in automation, robotics, and advanced separation chemistry is expected to further optimize recovery rates, ultimately supporting full circular integration of solar manufacturing and recycling ecosystems.

Challenges:

- High Cost and Limited Economic Viability of Recycling Operations: A major restraint in the Solar Panel Recycling Market is the high operational cost associated with dismantling, material separation, and purification of photovoltaic modules. The root cause lies in the complex multilayer structure of solar panels, which requires energy-intensive processes to extract low-volume but high-value materials such as silver and high-purity silicon. In many cases, recovery yields do not fully offset processing and logistics costs, particularly in regions without mature recycling infrastructure. Industrially, this cost burden limits large-scale adoption and discourages investment in dedicated recycling facilities. Commercially, it creates pricing pressure across the value chain, making recycled materials less competitive compared to virgin raw materials.

- Lack of Standardized Collection Systems and Reverse Logistics Infrastructure: Another critical challenge is the absence of globally standardized collection frameworks and efficient reverse logistics networks for end-of-life solar panels. The root cause stems from fragmented regulatory policies across regions and inconsistent enforcement of producer responsibility requirements. As a result, large volumes of decommissioned panels remain uncollected or are processed through informal waste channels. This fragmentation significantly impacts industry efficiency, as recyclers face unpredictable feedstock supply and high transportation costs. From a commercial perspective, it reduces scalability and deters long-term infrastructure investment due to uncertain input availability.

Solar Panel Recycling Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

16.5% |

| Base Year Market Size (2025) |

USD 366.2 million |

| Forecast Year Market Size (2035) |

USD 1,686.4 million |

| Regional Scope |

|

Solar Panel Recycling Market Segmentation Analysis:

Process Segment Analysis

The mechanical process segment is anticipated to garner the largest share of 68.3% in the solar panel recycling market by the end of 2035.

Factors such as cost efficiency, scalability, and the ability to recover high volumes of bulk materials such as glass, aluminum, and copper without complex chemical treatment. Current demand is primarily driven by the rising influx of decommissioned photovoltaic modules from utility-scale solar installations, where operators prioritize low-cost and high-throughput recycling solutions. As per the International Energy Agency, Photovoltaic Power Systems Programme (IEA-PVPS), crystalline silicon-based solar modules account for around 98% of global PV installations, reinforcing the dominance of mechanically recyclable panel types due to their standardized structure and high material recoverability. On the supply side, mechanical recycling benefits from relatively lower capital intensity compared to thermal and chemical alternatives, enabling faster deployment across emerging recycling hubs.

Type Segment Analysis

The monocrystalline type segment is projected to hold a considerable share in the solar panel recycling market during the forecast period.

The segment’s development is highly driven by its high material purity, superior energy efficiency, and increasing dominance in new photovoltaic installations. Current demand is primarily driven by the widespread deployment of monocrystalline solar modules in utility-scale and rooftop solar projects, as they deliver higher efficiency rates and longer operational lifespans compared to alternative technologies. As these panels reach end-of-life in the coming decades, their high silicon content makes them a valuable feedstock for advanced recycling systems focused on high-purity material recovery. Industry adoption trends are shifting toward recycling processes optimized specifically for monocrystalline silicon wafers, as recyclers aim to recover high-value silicon suitable for reuse in new PV cell manufacturing.

Our in-depth analysis of the global solar panel recycling market includes the following segments:

|

Segment |

Sub-segment |

|

Process |

|

|

Type |

|

|

Application |

|

Solar Panel Recycling Market Regional Insights:

Europe Market Trends & Insights:

Europe is projected to be the dominant region in the global solar panel market, capturing 71.1% of the total market value by 2035.

The region has maintained its leadership in the market based on three synergistic advantages, including regulatory stringency, infrastructural maturity, and first-mover industrial investment. The region's dominance is anchored by the Waste Electrical and Electronic Equipment (WEEE) Directive (2012/19/EU), which mandates extended producer responsibility for photovoltaic modules and establishes legally binding recovery and recycling targets. Under Germany's ElektroG, large photovoltaic modules must achieve a prescribed recovery rate of at least 85% and a preparation for reuse and recycling rate of at least 80%. This regulatory framework has catalyzed continuous investment in recycling infrastructure, thus positively impacting market growth.

Germany stands as Europe's most advanced national market, benefiting from the world's longest history of large-scale solar deployment and correspondingly mature waste management systems. The country's ElektroG framework imposes comprehensive producer obligations, including registration, financial guarantees for return and disposal, and mandatory product design for dismantling and recycling facilitation. Germany's recycling infrastructure is characterized by high compliance rates, established processing facilities, and robust industry participation. Crucially, German collection systems operate with clear consumer guidance, based on which defective solar modules are accepted free of charge at designated recycling centers under the Electrical and Electronic Equipment Act's take-back provisions.

The UK, while outside the regional regulatory framework, faces a comparable decommissioning imperative. According to peer-reviewed research conducted at the University of Birmingham, the UK's current PV capacity of approximately 18 GW corresponds to roughly 70 million installed modules. Cumulative end-of-life UK PV module numbers will exceed 100 million, representing approximately 2 million metric tons, by 2050. Critically, the study published in Energy Strategy Reviews in September 2025 demonstrates that the tonnage of UK solar waste is expected to exceed the current pan-European solar waste recycling capacity by 2035, demonstrating an urgent need for further investment in domestic recycling infrastructure. The research emphasizes that domestic processing would enable retention of high-value and critical materials within UK supply chains, positioning the country as both a significant waste generator and an emerging market for recycling capacity expansion.

North America Market Trends & Insights:

North America is considered the fastest-growing region in the solar panel recycling market.

The market development is supported by expanding solar energy deployment, increasing awareness of photovoltaic waste management, and growing emphasis on sustainable resource recovery. As large-scale solar projects installed over the past decade continue to mature, the region is witnessing greater attention toward end-of-life module management and circular economy practices. Industrial activity is increasing through investments in recycling facilities, material recovery technologies, and reverse logistics networks designed to handle future solar waste streams efficiently. Government agencies and industry stakeholders are also promoting responsible disposal and recycling practices through environmental sustainability programs and clean energy initiatives.

The U.S. market is defined by its fragmented yet rapidly formalizing regulatory environment. Absent comprehensive federal recycling mandates, states including California, New Jersey, North Carolina, and Washington have pioneered independent stewardship programs. This has created regional inconsistencies but also served as a policy laboratory. The anticipated EPA universal waste rule would harmonize requirements nationally, enabling recyclers to operate across state lines without navigating divergent regulations. Major utility owners are proactively developing decommissioning protocols, recognizing that upcoming replacement cycles for large-scale solar farms represent both logistical challenges and material recovery opportunities. The market's growth in the country is poised to be driven by the convergence of state leadership, federal rulemaking, and utility-scale repowering cycles.

The solar panel recycling market in Canada operates at smaller scale but benefits from alignment with North American clean energy supply chains and provincial-level waste management initiatives. Canada's solar capacity is concentrated in Ontario, Alberta, and British Columbia, where provincial environmental regulations increasingly address end-of-life PV management. The country's proximity to U.S. recycling infrastructure offers near-term processing access, though domestic capacity expansion is underway. Canada's opportunity lies in developing specialized capabilities for thin-film modules, where certain provinces have unique installed bases, and in integrating PV recycling into broader circular economy frameworks for electronics and construction materials.

Leading Companies Operating in the Solar Panel Recycling Market:

The solar panel recycling market is characterized by a mix of specialized photovoltaic recycling companies, waste management providers, and renewable energy technology firms focused on material recovery and circular economy solutions. Competition is centered on recycling efficiency, recovery rates for valuable materials such as silicon and silver, proprietary processing technologies, and compliance with evolving environmental regulations. Leading participants are expanding their recycling capacity, forming partnerships with solar manufacturers and utilities, and investing in advanced material separation technologies

Here is a list of key players operating in the global solar panel recycling market:

|

Company |

Specialty |

HQ |

Position |

|

Veolia |

Solar panel recycling and resource recovery |

France |

Leader |

|

ROSI |

High-purity silicon and silver recovery |

France |

Major |

|

First Solar |

Closed-loop PV module recycling |

U.S. |

Leader |

|

Reiling Group |

Glass and photovoltaic recycling |

Germany |

Major |

|

PV CYCLE |

Collection and recycling compliance services |

Belgium |

Major |

|

Solarcycle |

End-of-life solar module processing |

U.S. |

Major |

|

SoliTek |

Sustainable solar manufacturing and recycling initiatives |

Lithuania |

Niche |

|

Rinovasol |

Reuse, refurbishment, and recycling solutions |

Germany |

Niche |

|

Veolia |

Solar panel recycling and resource recovery |

France |

Leader |

Recent Developments

- In April 2026, ROSI strengthened its position as a leading Europe-based player in high-value solar panel recycling, announcing over €20 million in funding to accelerate its industrial expansion across Europe.

- In February 2026, Comstock Inc. and its subsidiary, Comstock Metals LLC, introduced its facility in Kings County and received approval from California’s Department of Toxic Substances Control, and has been placed on a very select list of companies authorized as universal waste recyclers that can treat photovoltaic modules.

- In May 2025, SOLARCYCLE signed a Recycling Services Agreement with RWE Clean Energy to ensure the sustainable recycling of solar panels from many of RWE’s solar energy projects at the end of their operational life, supporting RWE’s commitment to building a circular and zero-waste solar economy in the U.S. while working to ensure America’s growing energy demand.

Frequently Asked Question

In 2025, the solar panel recycling market exceeded USD 366.2 million.

The solar panel recycling market is projected to reach USD 1,686.4 million by the end of 2035, expanding at a CAGR of 16.5% over the forecast period (2026-2035).

The major players in the market are Veolia, ROSI, First Solar, Reiling Group, PV CYCLE, Solarcycle, SoliTek, Rinovasol, and others.

In the Process segment, the Mechanical Process sub-segment is anticipated to capture the largest market share of 68.3% in the future and exhibit lucrative growth opportunities during 2026-2035. This growth trajectory is largely attributed to its cost efficiency, scalability, and widespread adoption for recovering glass, aluminum, and other valuable materials from end-of-life photovoltaic modules.

Europe is projected to hold the largest market share of 71.1% by the end of 2035 and provide more business opportunities in the future. Continuous investments in solar waste management infrastructure and strong regulatory support across Germany and the UK are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1009 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy