Report ID: 1010 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Power Semiconductor Market Market Outlook:

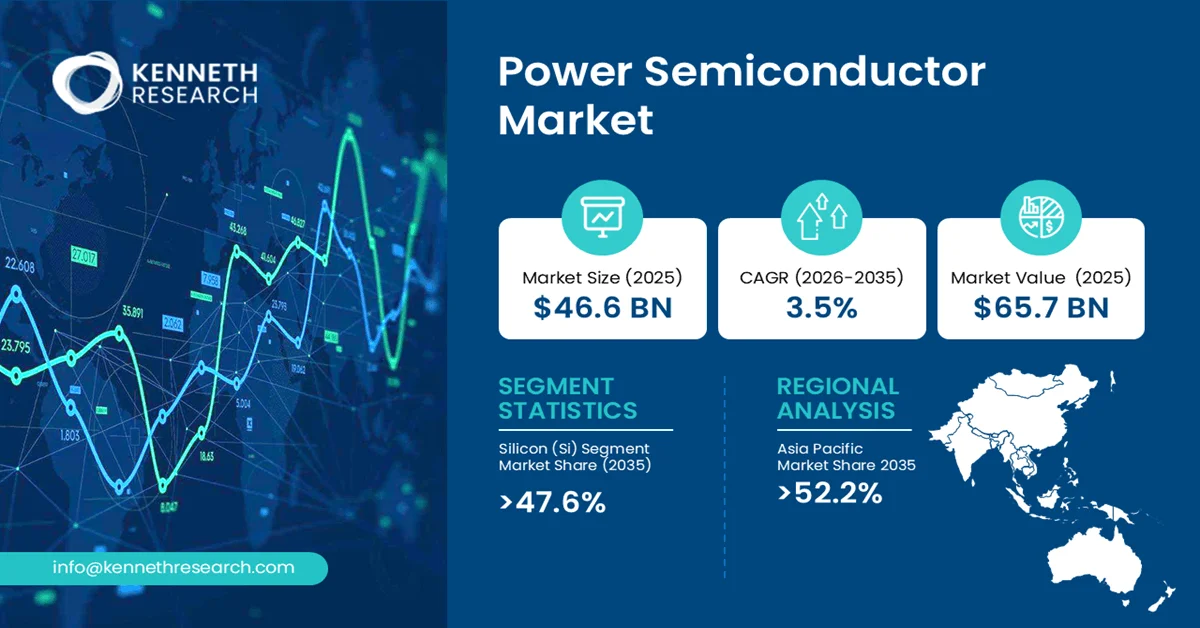

The global power semiconductor market size was valued at USD 46.6 billion in 2025 and is projected to reach USD 48.2 billion in 2026. In addition, the home improvement industry is further expected to be worth USD 65.7 billion by the end of 2035, rising at a CAGR of 3.5% during the forecast period, i.e., 2026-2035.

The primary growth driver of the power semiconductor market is the accelerating global transition toward electrification and energy efficiency. Rising deployment of electric vehicles, renewable energy systems, industrial automation equipment, and advanced power infrastructure is increasing demand for high-performance semiconductor devices capable of efficient power conversion, management, and control.

Power semiconductors are specialized electronic components designed to control, convert, and manage electrical power in systems ranging from industrial drives to consumer electronics. Key characteristics include high breakdown voltage, low on-state resistance, fast switching capability, and thermal resilience. These components are fundamental to power supplies, motor drives, battery chargers, inverters, and grid infrastructure. Industrial relevance has intensified as global energy consumption patterns shift. The International Energy Agency (IEA) reports that global electricity demand rose 4.4% in 2024, with wind and solar photovoltaic generation expected to cover over 90% of additional demand growth in 2025. This renewable energy expansion requires sophisticated power conversion systems, where power semiconductors serve as the core switching elements in grid-tied inverters, maximum power point trackers, and energy storage systems.

Key Power Semiconductor Market Insights Summary:

Key Takeaways: Market Trends & Insights

- In the material type segment, the silicon (Si) sub-segment is anticipated to capture the revenue share of 47.6% during 2026-2035

- The Asia Pacific power semiconductor market is projected to hold the largest revenue share of 52.2% by the end of 2035

- The major players in the market are STMicroelectronics, Mitsubishi Electric, Toshiba Electronic Devices & Storage, ROHM Semiconductor, Texas Instruments, and others.

Market Drivers

- Expansion of renewable energy generation and grid modernization projects

- Rising electrification of transportation and charging infrastructure deployment

- Increasing adoption of industrial automation and smart manufacturing systems

- Growing demand for energy-efficient power management across data centers and telecommunications infrastructure

Challenges

- Supply Chain Complexity and Dependence on Specialized Semiconductor Materials

- High Qualification Requirements and Extended Product Commercialization Cycles

Power Semiconductor Market Overview & Supply Chain

The power semiconductor industry value chain begins with the sourcing of raw materials and specialty inputs, including silicon wafers, silicon carbide substrates, gallium nitride materials, specialty gases, photoresists, and semiconductor-grade chemicals. The manufacturing stage involves wafer processing, semiconductor fabrication, device design, assembly, packaging, and testing. Integrated device manufacturers, foundries, and outsourced semiconductor assembly and test providers collaborate to produce power diodes, transistors, modules, and integrated power management components that meet stringent performance and reliability requirements.

Following production, products are distributed through direct sales channels, authorized distributors, electronics component suppliers, and system integrators. The downstream ecosystem includes original equipment manufacturers and industrial system developers that incorporate power semiconductors into finished products. Key end users span automotive, industrial automation, renewable energy, consumer electronics, telecommunications, aerospace, and power infrastructure sectors. Major stakeholders across the value chain include raw material suppliers, wafer manufacturers, semiconductor foundries, packaging and testing providers, distributors, technology developers, equipment suppliers, OEMs, and end-use industries.

Power Semiconductor Market: Growth Drivers & Challenges

Growth Drivers:

- Expansion of Renewable Energy Infrastructure and Power Conversion Requirements: The accelerating deployment of renewable energy systems is creating substantial demand for power semiconductor technologies. Solar photovoltaic installations, wind turbines, battery energy storage systems, and grid-connected renewable assets rely on power semiconductors for power conversion, voltage regulation, switching, and energy management functions. As utilities and governments prioritize clean energy integration, the need for highly efficient power electronics continues to increase across generation, transmission, and distribution networks. Supporting this trend, the International Energy Agency (IEA) reported that global annual renewable capacity additions are projected to increase from 666 GW in 2024 to almost 935 GW by 2030, highlighting the growing need for power conversion and control technologies across renewable energy systems.

- Increasing Electrification Across Industrial and Transportation Systems: The global transition toward electrified industrial operations and transportation systems is significantly increasing the utilization of power semiconductors. Electric drivetrains, industrial motor controls, robotics, factory automation equipment, and intelligent power distribution systems all require advanced semiconductor devices to optimize power flow, reduce energy losses, and improve operational reliability. As manufacturers pursue greater productivity, energy efficiency, and operational flexibility, power semiconductors are becoming critical enabling technologies within modern industrial ecosystems. The shift toward digitally connected infrastructure further reinforces demand for sophisticated power management solutions capable of supporting complex and high-performance electrical architectures.

Challenges:

- Supply Chain Complexity and Dependence on Specialized Semiconductor Materials: The power semiconductor industry relies on a highly specialized supply chain involving semiconductor-grade wafers, advanced substrates, fabrication equipment, packaging materials, and precision manufacturing processes. The increasing adoption of advanced materials such as silicon carbide and gallium nitride has further intensified dependence on a limited number of qualified suppliers. Any disruption in raw material availability, manufacturing capacity, logistics networks, or geopolitical trade conditions can affect production schedules and component availability. From an industry perspective, supply constraints can delay product development programs, increase procurement risks, and create uncertainty for downstream manufacturers.

- High Qualification Requirements and Extended Product Commercialization Cycles: Power semiconductor devices are deployed in mission-critical applications where reliability, safety, thermal performance, and long operational lifecycles are essential. As a result, products must undergo rigorous design validation, certification, testing, and qualification procedures before commercial deployment. Industries such as automotive, industrial automation, aerospace, energy infrastructure, and telecommunications often maintain strict technical requirements that can significantly lengthen product approval timelines. This challenge affects industry innovation cycles by increasing development complexity and delaying the introduction of new technologies into commercial applications.

Power Semiconductor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

3.5% |

| Base Year Market Size (2025) |

USD 46.6 billion |

| Forecast Year Market Size (2035) |

USD 65.7 billion |

| Regional Scope |

|

Power Semiconductor Market Segmentation Analysis:

Material Type Segment Analysis

The silicon (Si) segment, part of the material type, is anticipated to garner the largest share of 47.6% in the power semiconductor market by the end of 2035.

The aspect of its mature manufacturing ecosystem, cost efficiency, and proven reliability across high-volume power electronics applications. Current demand is driven by its extensive use in electric vehicle powertrains, industrial motor drives, renewable energy inverters, and consumer power supply units, where scalable and cost-effective power conversion remains essential. On the supply side, silicon benefits from a globally optimized value chain encompassing abundant raw material availability, standardized wafer processing, and well-developed packaging and testing ecosystems. According to the International Energy Agency (IEA), global electricity consumption in data centres is projected to reach nearly 1,000 TWh by 2026, driven by electrification and digital infrastructure growth, reinforcing long-term demand for efficient silicon-based power conversion systems.

Product Form Segment Analysis

The discrete power semiconductor devices segment, which is under the product form, is projected to hold a considerable share during the forecast period.

Discrete power semiconductor devices are expected to experience strong growth due to increasing demand for flexible, application-specific power management solutions across automotive, industrial, and energy systems. Current demand is driven by their extensive use in electric vehicle powertrains, onboard charging systems, industrial motor control, renewable energy inverters, and fast-charging infrastructure, where precise switching and voltage regulation are essential. From a supply-side perspective, discrete devices benefit from well-established manufacturing ecosystems, relatively lower design complexity compared to integrated modules, and broad availability across global semiconductor fabrication networks. This enables faster production scaling and shorter design cycles for OEMs across automotive and industrial sectors.

Our in-depth analysis of the global power semiconductor market includes the following segments:

|

Segment |

Sub-segment |

|

Material Type |

|

|

Product Form |

|

|

Application |

|

Power Semiconductor Market Regional Insights:

Asia Pacific Market Trends & Insights:

The Asia Pacific maintains its position as the dominant region in the global power semiconductor market, capturing 52.2% of total market value by 2035.

This is highly driven by concentrated manufacturing ecosystems, robust domestic consumption, and sustained government-backed investment in semiconductor self-sufficiency. Regulatory support across multiple Asia Pacific economies has accelerated capacity expansion, with Japan, China, and South Korea each implementing targeted subsidy programs to reduce import dependence and secure supply chains for power semiconductors designated as critical infrastructure components. Besides, under the Supply Assurance Plan approval, METI has allocated support for Kaga Toshiba Electronics Corporation's Nomi City facility, targeting 420,000 12-inch equivalent wafers annually for silicon power semiconductor production commencing March 2025. This government-backed capacity expansion exemplifies the region's coordinated approach to maintaining global leadership.

China dominates the power semiconductor market consumption, driven by the world's largest electric vehicle market, expansive industrial automation sector, and strategic push for semiconductor self-reliance. The national power device demand is further amplified by massive renewable energy installations that require grid-tied inverters and power conversion systems. Domestic power semiconductor suppliers, including StarPower and CRRC Times Electric, have gained share in medium-voltage IGBT modules for locomotives and industrial drives, while government subsidies encourage automotive OEMs to prioritize locally sourced power components.

Japan maintains leadership in power semiconductor production despite its consumption trailing that of China. Domestic suppliers, such as Mitsubishi Electric, Fuji Electric, Toshiba, Rohm, and Denso, collectively hold significant global market share. METI’s consolidation strategy aims to create larger, more competitive entities capable of matching China-based and Western investments in wide bandgap capacity. With established 200mm silicon lines and aggressive SiC expansion at Miyazaki Prefecture's Koyu District facility, targeting 720,000 8-inch equivalent wafers annually for SiC power semiconductors from April 2026, Japan is positioning itself as the premium manufacturing hub for advanced power devices serving automotive and industrial customers globally.

North America Market Trends & Insights:

North America is considered the fastest-growing region in the power semiconductor market.

The market’s development in the region is highly propelled by strong demand from electric mobility, renewable energy integration, industrial automation, and advanced computing infrastructure. The region benefits from a highly developed industrial base, significant investments in clean energy transition, and rapid expansion of data centers and electrified transport systems. Government initiatives such as semiconductor supply chain reshoring, energy transition funding programs, and incentives for domestic manufacturing are strengthening regional resilience and encouraging localized production of advanced power electronics. Future opportunities are expected to emerge from grid modernization projects, EV charging infrastructure expansion, and increased adoption of high-efficiency power conversion systems across industrial and commercial applications.

The United States is the primary contributor in the region, supported by large-scale investments in semiconductor manufacturing capacity, strong automotive electrification trends, and rapid growth in data center infrastructure. The country is also advancing domestic semiconductor ecosystem development through strategic policy support and R&D initiatives focused on next-generation power electronics.

Canada is gradually expanding its role through clean energy deployment, electric mobility initiatives, and growing participation in advanced manufacturing and semiconductor-related research activities. Canadian industrial strategy increasingly emphasizes energy efficiency and low-carbon technologies, creating long-term demand for efficient power semiconductor solutions across utilities and transportation sectors.

Leading Companies Operating in the Global Power Semiconductor Market:

The power semiconductor market is highly consolidated among a mix of global integrated device manufacturers and specialized power electronics companies. Competition is driven by technological innovation in wide-bandgap materials, manufacturing scale, and automotive-grade qualification capabilities. Leading players focus on expanding SiC and GaN portfolios, improving energy efficiency, and strengthening supply chain resilience through capacity expansion and strategic partnerships with automotive and industrial OEMs. The market also reflects strong vertical integration, where key companies control design, fabrication, and packaging to ensure performance reliability and cost efficiency across high-power applications.

Here is a list of key players operating in the global power semiconductor market:

|

Company |

Specialty |

HQ |

Position |

|

Infineon Technologies |

Power electronics and automotive semiconductors |

Germany |

Leader |

|

ON Semiconductor |

Energy-efficient power and sensing solutions |

U.S. |

Leader |

|

STMicroelectronics |

Mixed-signal and power semiconductor solutions |

Switzerland |

Leader |

|

Mitsubishi Electric |

Industrial and automotive power devices |

Japan |

Major |

|

Toshiba Electronic Devices & Storage |

Power semiconductors and discrete devices |

Japan |

Major |

|

ROHM Semiconductor |

SiC power devices and automotive electronics |

Japan |

Major |

|

Texas Instruments |

Analog and power management ICs |

U.S. |

Major |

|

Fuji Electric |

Industrial power semiconductor systems |

Japan |

Niche |

|

Littelfuse |

Circuit protection and power control devices |

U.S. |

Niche |

|

Infineon Technologies |

Power electronics and automotive semiconductors |

Germany |

Leader |

Recent Developments

- In June 2026, U.S. Department of Commerce announced the signing of a Direct Funding Agreement with Powerex to invest $30 million in manufacturing and R&D to dramatically expand domestic power module production.

- In February 2026, Navitas Semiconductor accelerated a strategic pivot to Navitas 2.0 with focus on GaN and high-voltage SiC solutions targeting high growth, high-power markets totaling $3.5 billion serviceable available market (SAM) in 2030.

Frequently Asked Question

In 2025, the power semiconductor market exceeded USD 46.6 billion.

The power semiconductor market is projected to reach USD 65.7 billion by the end of 2035, expanding at a CAGR of 3.5% over the forecast period (2026–2035).

The major players in the market are Infineon Technologies, ON Semiconductor, STMicroelectronics, Mitsubishi Electric, Toshiba Electronic Devices & Storage, ROHM Semiconductor, Texas Instruments, Fuji Electric, Littelfuse, and others.

In the material type segment, the silicon (Si) sub-segment is anticipated to capture the largest market share of 47.6% in the future and exhibit lucrative growth opportunities during 2026–2035. This dominance is attributed to its cost efficiency, mature manufacturing ecosystem, and widespread adoption across automotive, industrial, and energy applications.

The Asia Pacific is projected to hold the largest market share of 52.2% by the end of 2035 and provide more business opportunities in the future. Continuous expansion of electric vehicle manufacturing in China and advanced semiconductor and automotive electronics leadership in Japan are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1010 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy