Report ID: 1016 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Oncology Molecular Diagnostics Market Outlook:

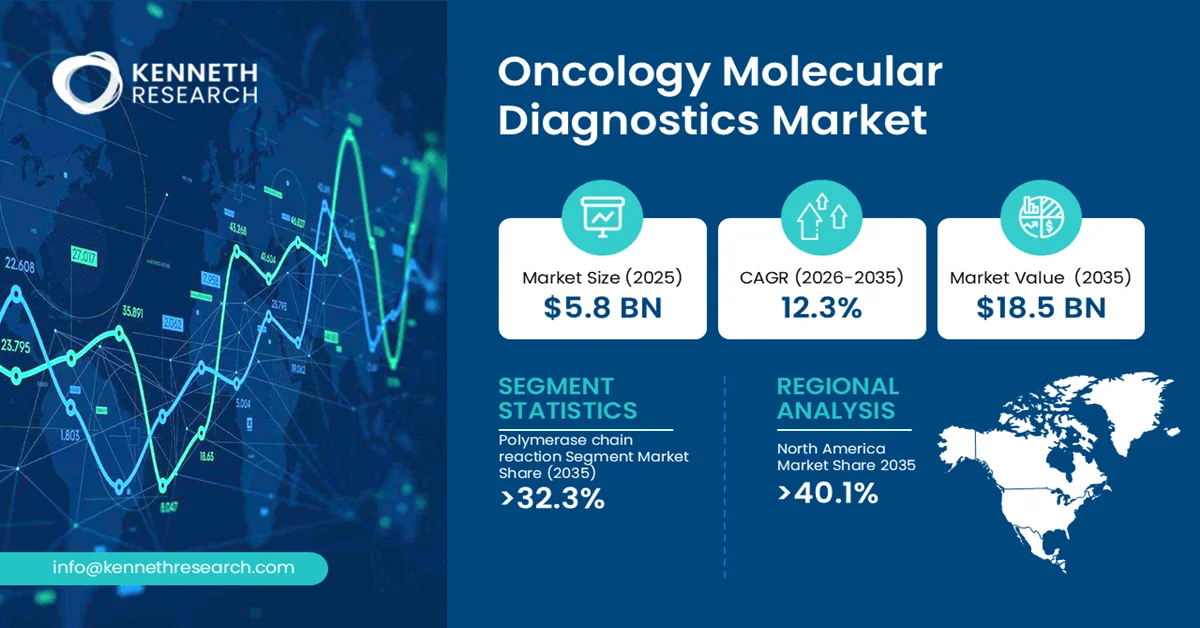

The global oncology molecular diagnostics market size was valued at USD 5.8 billion in 2025 and is projected to reach USD 6.5 billion in 2026. In addition, the ground surveillance radar systems industry is further expected to be worth USD 18.5 billion by the end of 2035, rising at a CAGR of 12.3% during the forecast period, i.e., 2026-2035.

The primary growth driver of the Oncology Molecular Diagnostics Market is the increasing global cancer burden and the growing adoption of precision medicine. Rising demand for early cancer detection, companion diagnostics, biomarker-based testing, and personalized treatment approaches is accelerating the use of molecular diagnostic technologies across healthcare systems worldwide.

The oncology molecular diagnostics market comprises technologies and assays used to detect cancer-related genetic alterations, biomarkers, mutations, and nucleic acid sequences for diagnosis, prognosis, treatment selection, and disease monitoring. These solutions include polymerase chain reaction (PCR), next-generation sequencing, fluorescence in situ hybridization, and other molecular techniques that enable highly sensitive and specific cancer detection. The market plays a critical role in precision oncology by supporting individualized therapeutic decisions and improving clinical outcomes.

Key Oncology Molecular Diagnostics Market Insights Summary:

Key Takeaways: Market Trends & Insights

- In the technology segment, the polymerase chain reaction sub-segment is anticipated to capture the revenue share of 32.3% during 2026-2035

- In the cancer type, the breast cancer segment is predicted to garner the revenue share of 25.2% by the end of the forecast duration

- North America oncology molecular diagnostics market is projected to hold the largest revenue share of 40.1% by the end of 2035

- The Asia Pacific in the oncology molecular diagnostics market is expected to grab a considerable share of 23.7% during the forecast period

- The major players in the market are Thermo Fisher Scientific Inc., Illumina, Inc., Agilent Technologies, Inc., and others

Market Drivers

- Rising global cancer burden and increasing emphasis on early detection

- Expansion of precision medicine and companion diagnostics

- Advancements in genomic technologies and biomarker discovery

- Growing integration of artificial intelligence and bioinformatics in oncology diagnostics

Challenges

- High complexity and cost associated with advanced molecular diagnostic technologies

- Regulatory and reimbursement uncertainties affecting commercialization and adoption

Oncology Molecular Diagnostics Market Overview & Supply Chain

The value chain of the oncology molecular diagnostics begins with the procurement of critical inputs, including reagents, enzymes, nucleic acid extraction kits, primers, probes, sequencing chemicals, antibodies, and laboratory consumables sourced from biotechnology and specialty chemical suppliers. Instrument manufacturers and software developers also contribute analytical platforms and bioinformatics tools required for molecular testing.

Production activities involve assay development, biomarker validation, kit manufacturing, quality control, and regulatory compliance processes undertaken by diagnostic companies and biotechnology firms. Finished products are distributed through direct sales channels, medical distributors, and laboratory service providers to healthcare facilities worldwide. Key end users include hospitals, clinical laboratories, cancer centers, academic research institutions, and pharmaceutical companies engaged in precision medicine and companion diagnostics development.

Oncology Molecular Diagnostics Market: Growth Drivers & Challenges

Growth Drivers:

- Rising Global Cancer Burden and Increasing Demand for Early Diagnosis: The growing incidence of cancer worldwide is accelerating the adoption of oncology molecular diagnostics. Healthcare providers are increasingly emphasizing early detection and personalized treatment approaches, creating strong demand for technologies capable of identifying genetic mutations and biomarkers with high sensitivity and specificity. According to the World Health Organization (WHO) and the International Agency for Research on Cancer (IARC), there were approximately 20 million new cancer cases globally in 2022, and this figure is projected to continue rising. The rising prevalence of disease is expected to reinforce long-term demand for advanced molecular testing platforms and accelerate innovation in cancer diagnostics.

- Expansion of Precision Medicine and Biomarker-Based Therapeutics: The growing adoption of precision medicine is transforming cancer management and creating substantial opportunities for oncology molecular diagnostics. Advances in genomics and biomarker research are enabling healthcare providers to tailor therapies according to individual genetic profiles, increasing treatment efficacy while minimizing adverse effects. Molecular diagnostic technologies have become indispensable in identifying actionable mutations and guiding the use of targeted therapies and immunotherapies. Simultaneously, improvements in sequencing technologies, automation, and bioinformatics are enhancing analytical capabilities and expanding clinical applications.

Challenges:

- High Complexity and Cost Associated with Advanced Molecular Diagnostic Technologies: The development and deployment of oncology molecular diagnostic solutions involve sophisticated technologies, specialized reagents, and highly trained personnel, resulting in significant operational and capital requirements. Complex workflows, stringent quality standards, and the need for advanced laboratory infrastructure increase the cost of implementing molecular testing, particularly in resource-constrained healthcare settings. These factors can limit accessibility and slow the adoption of advanced diagnostic platforms among smaller laboratories and healthcare providers.

- Regulatory and Reimbursement Uncertainties Affecting Commercialization and Adoption: The oncology molecular diagnostics industry operates within a highly regulated environment characterized by evolving approval requirements, clinical validation standards, and varying reimbursement frameworks across countries. Differences in regulatory pathways and payer policies often create challenges for manufacturers seeking timely commercialization and broad market access. Extensive evidence requirements and prolonged approval timelines can delay product launches and increase development costs. These uncertainties may discourage investment in novel diagnostic technologies and complicate strategic planning for both established companies and emerging developers.

Oncology Molecular Diagnostics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

12.3% |

| Base Year Market Size (2025) |

USD 5.8 billion |

| Forecast Year Market Size (2035) |

USD 18.5 billion |

| Regional Scope |

|

Oncology Molecular Diagnostics Market Segmentation Analysis:

Technology Segment Analysis

The polymerase chain reaction segment is anticipated to garner the largest share of 32.3% in the oncology molecular diagnostics market by the end of 2035.

PCR technology delivers high sensitivity and specificity for detecting actionable mutations while operating within standard laboratory infrastructure and staff expertise levels. From a health economics perspective, PCR-based assays offer lower per-test costs compared to sequencing platforms, making them accessible across diverse healthcare settings from centralized reference laboratories to hospital-based molecular pathology departments. A comparative study published in Clinica Chimica Acta (2023) evaluated digital PCR and droplet digital PCR systems for analyzing liquid biopsy samples from 22 patients with lung and colorectal cancer. The study demonstrated that PCR detected EGFR mutations in all 17 positive non-small cell lung cancer samples tested, while detecting RAS mutations in 19 of 22 colorectal cancer specimens. Importantly, mutations detected at ≤200 copies/mL were captured by PCR technology, establishing its clinical utility for low-abundance mutation detection

Cancer Type Segment Analysis

The breast cancer sub-segment is projected to hold a considerable share in the oncology molecular diagnostics market during the forecast period.

The sub-segment’s development is highly propelled by the significant clinical and economic burden associated with overtreatment in hormone-receptor-positive, HER2-negative early-stage breast cancer, which accounts for over 70% of diagnosed cases. Molecular diagnostic tests—including genomic assays such as Oncotype DX, EndoPredict, Prosigna, MammaPrint, and the Breast Cancer Index—quantify recurrence risk by evaluating multi-gene expression profiles from tumor tissue, generating risk scores that directly inform adjuvant chemotherapy decisions. The clinical mechanism driving demand is risk stratification: patients with low-risk scores can safely forgo chemotherapy without compromising survival outcomes, thereby avoiding unnecessary toxicity, whereas high-risk scores justify aggressive treatment.

Our in-depth analysis of the global oncology molecular diagnostics market includes the following segments:

|

Segment |

Sub-segment |

|---|---|

|

Technology |

|

|

Cancer Type |

|

|

Products |

|

|

End users |

|

Oncology Molecular Diagnostics Market Regional Insights:

North America Market Trends & Insights:

North America is projected to be the dominant region in the global oncology molecular diagnostics market, capturing 40.1% of the total market value by 2035.

The region benefits from the U.S. Food and Drug Administration's proactive framework for companion diagnostic device clearance, including the strategic proposal to reclassify certain CDx tests to Class II, which lowers commercialization barriers and accelerates market entry for novel assays. On the production side, North America hosts the global headquarters of leading diagnostic manufacturers, including Roche, Thermo Fisher Scientific, Illumina, and Guardant Health, supported by an extensive network of contract manufacturing organizations and specialized reagent suppliers concentrated in biotechnology hubs across California, Massachusetts, and Maryland.

The United States constitutes the largest single-country market within North America, characterized by a mature reimbursement landscape and high test adoption rates across academic medical centers and community oncology practices. The U.S. market benefits from FDA approvals of companion diagnostics paired with novel targeted therapies, including the September 2025 approval of imlunestrant (INLURIYO™) for ESR1-mutated breast cancer, which simultaneously authorized the Guardant360 CDx assay as the required companion diagnostic device for patient identification. This regulatory paradigm—where therapeutic approval is contingent on diagnostic availability, creates mandatory testing volumes and predictable revenue streams for diagnostic manufacturers. The market is further supported by the National Cancer Institute's Surveillance, Epidemiology, and End Results (SEER) program, which tracks cancer incidence and mortality, providing population-level data that guides testing infrastructure investment.

Canada represents a smaller but growing market within North America, distinguished by its publicly funded healthcare system and centralized health technology assessment process through the Canadian Agency for Drugs and Technologies in Health (CADTH). Unlike the U.S. multi-payer system, Canadian market access is governed by provincial formularies and national reimbursement recommendations, creating a more consolidated but slower adoption pathway for novel molecular diagnostic tests. The market is characterized by concentrated testing volumes through major reference laboratories in Ontario, British Columbia, and Quebec, with academic medical centers in Toronto and Vancouver serving as regional hubs for comprehensive genomic profiling.

Asia Pacific Market Trends & Insights:

The Asia Pacific is considered the fastest-growing region in the oncology molecular diagnostics market by the end of the stipulated period.

The market’s development in the region is driven by rising cancer incidence, expanding middle-class healthcare expenditure, and deliberate government investment in precision medicine infrastructure. Market demand is propelled by the region's large and aging population, with cancer detection rates increasing as healthcare access expands beyond major metropolitan centers. Industrial activity is concentrated in diagnostic manufacturing hubs, with China emerging as a producer of PCR instruments and reagent kits, while Singapore and Malaysia host contract manufacturing organizations serving global diagnostic companies seeking supply chain diversification. Government initiatives across multiple Asia Pacific countries include national cancer screening programs, biomarker testing mandates for targeted therapy reimbursement, and investment in next-generation sequencing infrastructure at tertiary cancer centers.

China has rapidly evolved into the largest oncology molecular diagnostic market within Asia Pacific, driven by the National Medical Products Administration's clearance of domestically manufactured companion diagnostic tests and the inclusion of molecular testing in national cancer treatment guidelines. The market is characterized by concentrated testing volumes through major hospital-based laboratories and commercial reference laboratories, including Burning Rock Biotech, Genetron Health, and Amoy Diagnostics, which have developed PCR and next-generation sequencing panels targeting the most prevalent mutations in Chinese cancer patients.

Japan represents a mature, regulated oncology molecular diagnostic market distinguished by the Ministry of Health, Labour and Welfare's centralized companion diagnostic approval system, which requires simultaneous regulatory review of diagnostic tests alongside their paired therapeutic products under the Pharmaceuticals and Medical Devices Agency framework. This parallel approval mechanism creates predictable market access timelines and eliminates post-launch coverage uncertainty, as tests approved as companion diagnostics receive automatic National Health Insurance reimbursement at nationally standardized tariff rates.

Leading Companies Operating in the Global Oncology Molecular Diagnostics Market:

The oncology molecular diagnostics market is characterized by the presence of established diagnostics manufacturers, life sciences companies, and specialized genomics firms competing through technological innovation, product portfolio expansion, and strategic collaborations. Companies are focusing on advanced PCR platforms, next-generation sequencing technologies, companion diagnostics, and biomarker-based solutions to strengthen their market positions. Partnerships with pharmaceutical companies and research institutions are becoming increasingly important to support precision oncology initiatives and accelerate the development of personalized cancer diagnostics.

Here is a list of key players operating in the global oncology molecular diagnostics market:

|

Company |

Specialty |

HQ |

Position |

|

F. Hoffmann-La Roche Ltd. |

Molecular diagnostics and companion diagnostics |

Switzerland |

Leader |

|

QIAGEN N.V. |

Sample preparation and PCR technologies |

Netherlands |

Leader |

|

Thermo Fisher Scientific Inc. |

Genomic analysis and molecular testing solutions |

United States |

Leader |

|

Illumina, Inc. |

Next-generation sequencing platforms |

United States |

Major |

|

Agilent Technologies, Inc. |

Genomics and cancer biomarker solutions |

United States |

Major |

|

Bio-Rad Laboratories, Inc. |

PCR systems and molecular assays |

United States |

Major |

|

Danaher Corporation |

Precision diagnostics and life sciences technologies |

United States |

Major |

|

Myriad Genetics, Inc. |

Hereditary cancer and companion diagnostic testing |

United States |

Niche |

|

Guardant Health, Inc. |

Liquid biopsy and genomic profiling |

United States |

Niche |

Recent Developments

- In March 2026, Guardant Health, Inc. declared that the U.S. Food and Drug Administration (FDA) approved Guardant360® Liquid CDx, advancing blood-based comprehensive genomic testing by integrating genomic and epigenomic insights and helping clinicians make better-informed treatment selection decisions for patients with advanced cancer.

- In November 2024, Caris Life Sciences® proclaimed that the U.S. Food and Drug Administration (FDA) approved MI Cancer Seek™ for use as a companion diagnostic (CDx) to identify cancer patients who may benefit from treatment with targeted therapies.

- In May 2023, Foundation Medicine, Inc. received approval from the U.S. Food and Drug Administration (FDA) for FoundationOne®Liquid CDx to be used as a companion diagnostic for EXKIVITY® (mobocertinib), which is currently FDA-approved for adult patients with locally advanced or metastatic non-small cell lung cancer.

Frequently Asked Question

In 2025, the oncology molecular diagnostics market exceeded USD 5.8 billion.

The oncology molecular diagnostics market is projected to reach USD 18.5 billion by the end of 2035, expanding at a CAGR of 12.3% over the forecast period (2026-2035).

The major players in the market are F. Hoffmann-La Roche Ltd., QIAGEN N.V., Thermo Fisher Scientific Inc., Illumina, Inc., Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., Danaher Corporation, and others.

In the Technology segment, the Polymerase Chain Reaction (PCR) sub-segment is anticipated to capture the largest market share of 32.3% in the future and exhibit lucrative growth opportunities during 2026-2035. This growth trajectory is largely attributed to increasing demand for early cancer detection and the expanding adoption of precision medicine and biomarker-based diagnostics.

North America is projected to hold the largest market share of 40.1% by the end of 2035 and provide more business opportunities in the future. Continuous investments in precision medicine, genomic research, and advanced diagnostic technologies across the U.S. and Canada are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1016 |

Published Date: 15 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy