Report ID: 1014 |

Published Date: 16 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Dental Imaging Market Outlook:

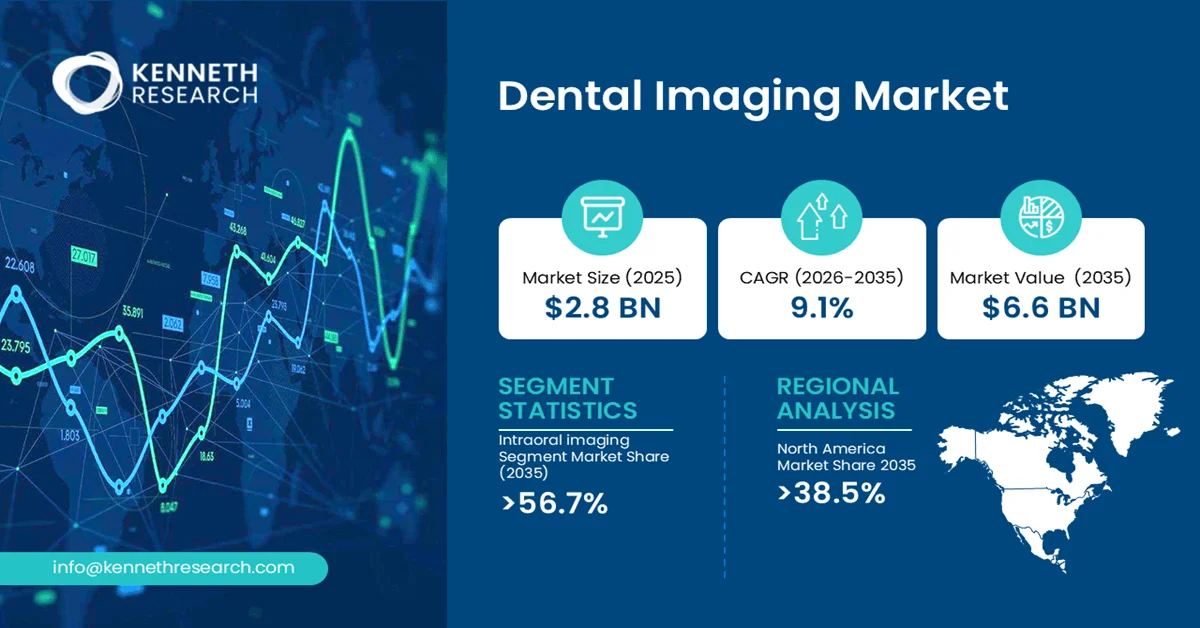

The global dental imaging market size was valued at USD 2.8 billion in 2025 and is projected to reach USD 3 billion in 2026. In addition, the ground surveillance radar systems industry is further expected to be worth USD 6.6 billion by the end of 2035, rising at a CAGR of 9.1% during the forecast period, i.e., 2026-2035.

The primary growth driver of the dental imaging market is the rising global burden of oral diseases and the increasing emphasis on early diagnosis and minimally invasive dental procedures. Growing adoption of digital imaging technologies, implantology treatments, orthodontics, and AI-enabled diagnostic systems is further accelerating demand worldwide.

Dental imaging encompasses a range of diagnostic technologies—including intraoral sensors, phosphor storage plate (PSP) systems, panoramic radiography, and cone-beam computed tomography (CBCT)—used for the detection, assessment, and treatment planning of oral health conditions. Key characteristics include the transition from film-based to digital capture, the integration of AI-assisted diagnostic algorithms, and the availability of both sensor-based (solid-state) and PSP-based receptor technologies, each offering distinct trade-offs between imaging speed, patient comfort, and image resolution. The industrial relevance of dental imaging lies in its foundational role across nearly all dental specialties: from caries detection in general practice to implantology planning, orthodontic simulations, endodontic assessment, and oral surgery navigation.

Key Dental Imaging Market Insights Summary:

Key Takeaways: Market Trends & Insights

- In the type segment, the intraoral imaging sub-segment is anticipated to capture the revenue share of 56.7% during 2026-2035

- In the application segment, the implantology segment is predicted to garner the revenue share of 31.6% by the end of the forecast duration

- North America in the dental imaging market is projected to hold the largest revenue share of 38.5% by the end of 2035

- The U.S. is predicted to garner a share of 76.4% in the regional dental imaging market

- The Asia Pacific in the dental imaging market is expected to grab a considerable share of 21.8% during the forecast period

- Japan is anticipated to account for 3.3% of the regional share in the dental imaging market

- The major players in the market are Vatech Co., Ltd., Acteon Group, Owandy Radiology, Midmark Corporation, Cefla S.C., and others

Market Drivers

- Increasing prevalence of oral diseases and age-related dental disorders worldwide.

- Expansion of dental healthcare infrastructure and specialized dental clinics.

- Rising adoption of cone-beam computed tomography (CBCT) and three-dimensional imaging solutions.

- Growing integration of digital workflows, artificial intelligence, and cloud-based dental platforms.

Challenges

- High Capital Investment and Ownership Costs

- Rising Demand for Implantology and Cosmetic Dental Procedures

Dental Imaging Market Overview & Supply Chain

The dental imaging market exhibits a multi-tiered value chain involving component suppliers, equipment manufacturers, distributors, healthcare providers, and technology developers. Raw material and input sources include semiconductor components, X-ray detectors, sensors, imaging software, electronic assemblies, optical systems, and specialized metals and plastics used in device production. Manufacturers integrate these components to develop digital radiography systems, cone-beam computed tomography (CBCT) units, panoramic imaging systems, and intraoral scanners while ensuring compliance with medical device regulations and quality standards.

Distribution activities are carried out through direct sales networks, authorized distributors, dental equipment suppliers, and e-commerce channels that support product availability across developed and emerging markets. End users primarily comprise dental clinics, hospitals, academic institutions, diagnostic centers, and specialty dental practices. Major stakeholders include component suppliers, imaging equipment manufacturers, software developers, regulatory authorities, healthcare providers, distributors, and service providers involved in installation, maintenance, and technical support, collectively contributing to the efficient delivery of advanced dental diagnostic solutions.

Dental Imaging Market: Growth Drivers & Challenges

Growth Drivers:

- Advancements in Digital and AI-Enabled Imaging Technologies: Continuous innovation in digital dentistry is emerging as a major catalyst for the dental imaging market. The transition from conventional radiography to digital imaging platforms, cone-beam computed tomography (CBCT), and cloud-connected intraoral scanners is improving diagnostic accuracy and workflow efficiency. Industry participants are also introducing advanced solutions that integrate software and connectivity capabilities. In September 2024, Dentsply Sirona launched Primescan® 2 powered by DS Core, described as the first cloud-native intraoral scanning solution, enabling scanning on any internet-connected device. Such innovations are expected to accelerate digital transformation and expand the use of advanced imaging systems in restorative and implant dentistry over the coming years.

- Rising Demand for Implantology and Cosmetic Dental Procedures: Growing patient awareness regarding oral aesthetics and restorative treatments is supporting demand for advanced dental imaging systems. Implantology procedures require highly accurate visualization of anatomical structures, making three-dimensional imaging and intraoral scanning indispensable tools for clinicians. Similarly, orthodontics and cosmetic dentistry increasingly rely on digital workflows to improve treatment precision and patient outcomes. The expanding preference for minimally invasive procedures and personalized treatment planning is encouraging dental professionals to invest in sophisticated imaging technologies.

Challenges:

- High Capital Investment and Ownership Costs: The high acquisition and lifecycle costs associated with advanced dental imaging systems represent a significant restraint for the market. Technologies such as cone-beam computed tomography (CBCT) systems, digital radiography platforms, and intraoral scanners require substantial upfront investments, in addition to ongoing expenses related to software upgrades, maintenance, calibration, and operator training. These financial barriers are particularly pronounced among small and independent dental clinics, especially in emerging economies where healthcare budgets remain constrained.

- Stringent Regulatory Compliance and Radiation Safety Requirements: The dental imaging industry operates within a highly regulated environment characterized by rigorous approval procedures, quality standards, and radiation safety requirements. Manufacturers must comply with various regional regulations concerning device performance, cybersecurity, software validation, and patient safety. The regulatory burden also necessitates continuous investments in compliance, documentation, and post-market surveillance activities. In the future, the growing incorporation of artificial intelligence, cloud connectivity, and digital health solutions is expected to introduce additional regulatory considerations, requiring companies to adopt more sophisticated compliance strategies and invest in advanced quality management capabilities.

Dental Imaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

9.1% |

| Base Year Market Size (2025) |

USD 2.8 billion |

| Forecast Year Market Size (2035) |

USD 6.6 billion |

| Regional Scope |

|

Dental Imaging Market Segmentation Analysis:

Type Segment Analysis

The intraoral imaging segment is anticipated to garner the largest share of 56.7% in the dental imaging market by the end of 2035.

The primary demand driver for intraoral imaging is the clinical necessity of detecting and monitoring dental caries across all patient populations. Government surveillance data from the U.S. Centers for Disease Control and Prevention (CDC) confirms that dental caries remains widespread: 46% of children aged 2 through 19 years have dental caries in one or more primary or permanent teeth. For each caries lesion detected, intraoral radiographs are standard-of-care for confirming clinical findings, assessing lesion depth, and determining proximity to the pulp. The prevalence increases with age, meaning older children and adolescents require ongoing radiographic surveillance, and decreases with higher family income, indicating that public health dental programs serving lower-income populations have sustained imaging needs.

Application Segment Analysis

The implantology sub-segment is projected to hold a considerable share in the dental imaging market during the forecast period.

The sub-segment’s robust growth is attributed to increasing demand for tooth replacement procedures, rising awareness regarding oral aesthetics, and the expanding elderly population susceptible to tooth loss. Implant procedures require precise visualization of bone structures and surrounding anatomy, making advanced dental imaging technologies indispensable for treatment planning and surgical accuracy. The growing preference for minimally invasive and customized restorative solutions is further stimulating demand for implant-related imaging applications.

Our in-depth analysis of the global dental imaging market includes the following segments:

|

Segment |

Sub-segment |

|

Type |

|

|

Application |

|

|

End user |

|

Dental Imaging Market Regional Insights:

North America Market Trends & Insights:

North America maintains its leadership position in the global dental imaging market, capturing 38.5% of the market in 2035.

This dominance is anchored by a well-established healthcare infrastructure and a high adoption rate of advanced medical technologies, including digital radiography and cone-beam computed tomography (CBCT) systems. The region benefits from a significant concentration of dental professionals who prioritize innovation and invest in cutting-edge diagnostic imaging solutions. Regulatory bodies such as Health Canada and the FDA maintain frameworks that balance safety oversight with market access, supporting continuous technology integration. The region also benefits from substantial public health investment: the Canadian Dental Care Plan (CDCP), launched in 2023, is expected to increase patient demand for oral health services, indirectly driving utilization of diagnostic imaging.

The United States represents the largest national market share within North America, driven by rapid advances in digital and clinical dental technologies and a growing burden of oral health disorders. The U.S. benefits from favorable healthcare reimbursement policies that encourage the adoption of CBCT and digital radiography. However, approximately 57 million people live in dental professional shortage areas, with 67% of these located in rural regions, creating demand for portable and teledentistry-integrated imaging solutions. The increasing demand for cosmetic dental procedures and expanding dental tourism further support adoption of modern diagnostic equipment nationwide. Key industry players, including Carestream Dental, Dentsply Sirona, Envista Holdings, and Midmark Corporation, maintain substantial U.S. operations, reinforcing domestic manufacturing and distribution networks.

Canada's dental imaging market is regulated by Health Canada, which oversees safety and performance standards for X-ray machines, CBCT units, and intraoral sensors. The market is poised for expansion due to advancements in digital radiography and 3D imaging systems enhance diagnostic capabilities and support treatment planning for implantology and orthodontics. Second, the Canadian Dental Care Plan (CDCP)—providing coverage to residents with adjusted family net income below CAD 90,000 without private insurance—is expected to significantly increase patient demand for oral health care services. According to provisional data from Statistics Canada's 2023 Survey of Oral Health Care Providers, 62% of practices surveyed reported capacity to accommodate additional patient visits, suggesting supply-side readiness for increased imaging volumes.

Asia Pacific Market Trends & Insights:

The Asia Pacific is considered to emerge as the fastest-growing region in the dental imaging market by the end of the forecast duration.

The market’s development in the region is propelled by rising demand for advanced oral healthcare services, expanding dental infrastructure, and increasing awareness regarding preventive and cosmetic dentistry. Growing industrial activity in medical device manufacturing and digital healthcare is encouraging the adoption of sophisticated diagnostic technologies across hospitals and specialized dental clinics. Governments across the region are promoting healthcare modernization and expanding access to oral health services, creating favorable conditions for the deployment of digital radiography systems, cone-beam computed tomography (CBCT), and intraoral scanners.

Japan holds the largest share within the Asia Pacific dental imaging market, reflecting a highly developed healthcare system, advanced dental industry, and one of the world's most rapidly aging populations. Key drivers include an aging society requiring increased restorative, implant, and periodontal care, as well as strong government support for preventive dentistry and oral health management through the national health insurance framework. The presence of leading domestic imaging manufacturers—including Morita Corporation, Asahi Roentgen, Yoshida Dental, and J. Morita Mfg. Corp.—ensures robust industrial activity and continuous innovation in low-dose CBCT and panoramic systems. Regulatory oversight by the Pharmaceuticals and Medical Devices Agency (PMDA) ensures high safety and performance standards, which domestic manufacturers meet through rigorous quality systems.

China's dental imaging market is shaped by a vast population, a rapidly aging demographic profile, and increasing prevalence of oral diseases linked to dietary changes. The country has witnessed accelerated adoption of CBCT technology, driven by rising demand for implantology and orthodontic treatments among the growing middle class. Government policies under the Healthy China 2030 framework are actively expanding oral healthcare access, including equipment procurement for public hospitals and community dental clinics. The market is increasingly characterized by tiered demand: first-tier cities (Beijing, Shanghai, Guangzhou) require premium CBCT and AI-integrated systems, while lower-tier cities and rural areas represent growth opportunities for portable and entry-level digital radiography solutions.

Leading Companies Operating in the Global Dental Imaging Market:

The dental imaging market is characterized by the presence of established medical device manufacturers and specialized digital dentistry companies competing through technological innovation, product portfolio expansion, software integration, and strategic collaborations. Leading companies leverage extensive distribution networks and strong research and development capabilities, while niche players concentrate on specialized imaging solutions and digital dentistry applications.

Here is a list of key players operating in the global dental imaging market:

|

Company |

Specialty |

HQ |

Position |

|

Dentsply Sirona |

Digital dentistry and dental imaging systems |

United States |

Leader |

|

Envista Holdings Corporation (KaVo Dental) |

Imaging equipment and dental technologies |

United States |

Leader |

|

Carestream Dental LLC |

Digital radiography and imaging software |

United States |

Major |

|

Planmeca Oy |

CBCT systems and digital dental solutions |

Finland |

Major |

|

Vatech Co., Ltd. |

Dental X-ray and three-dimensional imaging systems |

South Korea |

Major |

|

Acteon Group |

Dental imaging and ultrasonic technologies |

France |

Major |

|

Owandy Radiology |

Digital radiography and intraoral imaging solutions |

France |

Niche |

|

Midmark Corporation |

Imaging systems and dental workflow solutions |

United States |

Niche |

|

Cefla S.C. |

Dental diagnostic and imaging equipment |

Italy |

Niche |

Recent Developments

- In April 2026, DEXIS, a global leader in dental imaging, today announced the launch of DEXIS AI Month, a new initiative designed to expand access to its FDA cleared artificial intelligence technology and accelerate adoption of AI-powered diagnostics in dentistry.

- In March 2026, Dentsply Sirona and Siemens Healthineers are pleased to announce that the first-ever dental-dedicated MRI1 (ddMRI) system – MAGNETOM Free.Max Dental Edition – has received FDA clearance in the United States. This milestone follows the completion of a clinical trial2 validating the system’s significant potential across multiple dental specialties.

- In October 2024, Relu, a pioneer in artificial intelligence (AI) assisted segmentation for dental labs and software companies, proudly announces the dual achievement of 510(k) clearance by the U.S. Food and Drug Administration (FDA) and CE Mark approval by an EU Notified Body.

Frequently Asked Question

In 2025, the dental imaging market exceeded USD 2.8 billion.

The dental imaging market is projected to reach USD 6.6 billion by the end of 2035, expanding at a CAGR of 9.1% over the forecast period (2026-2035).

The major players in the market are Dentsply Sirona, Envista Holdings Corporation (KaVo Dental), Carestream Dental LLC, Planmeca Oy, Vatech Co., Ltd., J. Morita Corporation, and others.

In the Type segment, the Intraoral Imaging sub-segment is anticipated to capture the largest market share of 56.7% in the future and exhibit lucrative growth opportunities during 2026-2035. This growth trajectory is largely attributed to increasing adoption of digital dentistry and rising demand for accurate and low-radiation diagnostic imaging technologies.

North America is projected to hold the largest market share of 38.5% by the end of 2035 and provide more business opportunities in the future. Continuous investments in advanced dental technologies and strong adoption of digital imaging solutions across the U.S. and Canada are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1014 |

Published Date: 16 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy