Report ID: 1015 |

Published Date: 16 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Cancer Vaccine Market Outlook:

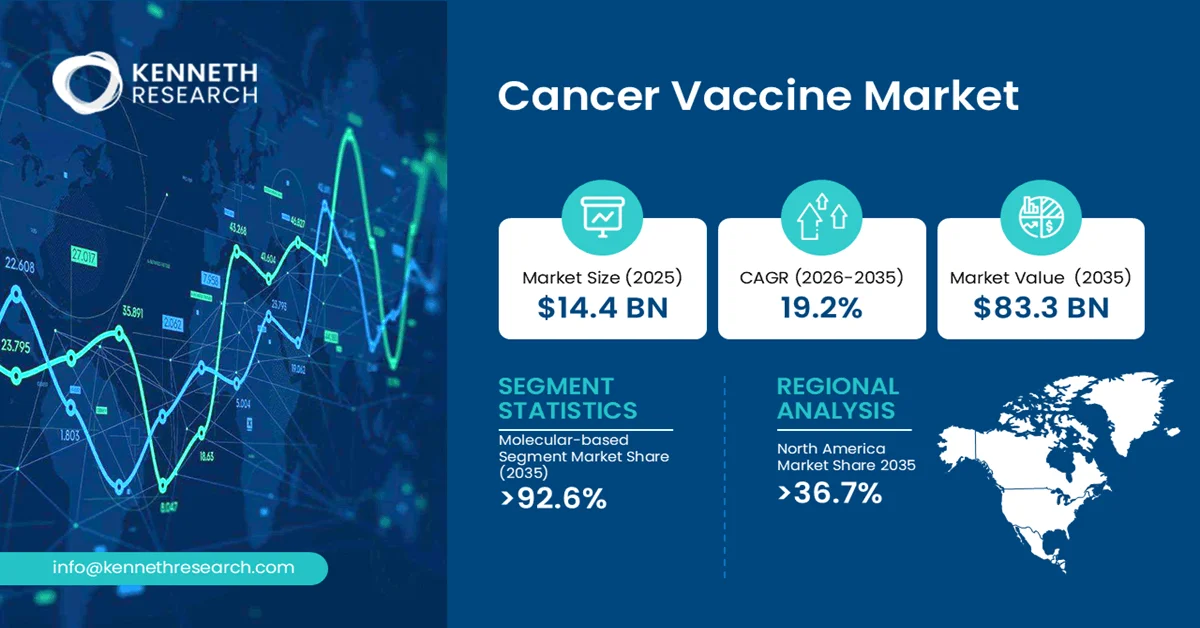

The global cancer vaccine market size was valued at USD 14.4 billion in 2025 and is projected to reach USD 17.1 billion in 2026. In addition, the ground surveillance radar systems industry is further expected to be worth USD 83.3 billion by the end of 2035, rising at a CAGR of 19.2% during the forecast period, i.e., 2026-2035.

The Cancer Vaccine Market is primarily driven by rising global cancer incidence, increasing immuno-oncology adoption, and advances in molecular-based vaccine platforms. Strong government funding for cancer immunization research and expanding clinical pipelines for preventive and therapeutic vaccines are accelerating commercialization and boosting global demand across developed and emerging healthcare systems.

The Cancer Vaccine Market refers to the development, production, and commercialization of biological formulations designed to prevent or treat cancer by stimulating the body’s immune system to recognize and eliminate cancerous cells. These vaccines are broadly categorized into preventive vaccines, which target virus-induced cancers such as HPV-related cervical cancer, and therapeutic vaccines, which are designed to treat existing malignancies by enhancing tumor-specific immune responses. It holds significant industrial relevance within the broader oncology and immunotherapy ecosystem due to its integration with precision medicine and biotechnology advancements.

Key Cancer Vaccine Market Insights Summary:

Key Takeaways: Market Trends & Insights

- In the technology segment, the molecular-based sub-segment is anticipated to capture the revenue share of 92.6% during 2026-2035

- In the type segment, the preventive sub-segment is predicted to garner the revenue share of 91.8% by the end of the forecast duration

- North America in the cancer vaccine market is projected to hold the largest revenue share of 36.7% by the end of 2035

- The U.S. is predicted to garner a share of 86.5% in the regional cancer vaccine market

- The Asia Pacific in the cancer vaccine market is expected to grab a considerable share of 29.9% during the forecast period

- Japan is anticipated to account for 2.9% of the regional share in the cancer vaccine market

- The major players in the market are GSK, Roche, Bristol Myers Squibb, Pfizer, CureVac, and others

Market Drivers

- Clinical Validation of mRNA–Checkpoint Inhibitor Combinations

- Expansion of mRNA-Based and Personalized Cancer Vaccine Platforms

- Increasing investment in combination immunotherapy approaches (vaccines + checkpoint inhibitors)

- Strong growth in biotechnology R&D funding and clinical trial expansion across oncology vaccines

Challenges

- High Clinical Validation Complexity and Tumor Heterogeneity

- Manufacturing and Scalability Constraints in Personalized Vaccine Production

Cancer Vaccine Market Overview & Supply Chain

The industry value chain of the Cancer Vaccine Market is a multi-stage ecosystem spanning biological input sourcing, advanced biomanufacturing, and specialized clinical delivery networks. It begins with raw materials such as antigenic peptides, recombinant proteins, viral vectors, plasmid DNA, and mRNA constructs derived from research laboratories and biotechnology input suppliers. These inputs are developed into vaccine candidates through preclinical research and translational studies.

Distribution relies heavily on temperature-controlled cold-chain logistics and specialized pharmaceutical distributors to maintain biological stability. End users primarily include oncology hospitals, cancer treatment centers, and research institutes conducting immunotherapy programs. Key stakeholders include biotech innovators, contract research organizations (CROs), and regulatory bodies such as the U.S. Food and Drug Administration, the National Cancer Institute, and global health authorities like the World Health Organization, which collectively shape approval pathways, clinical validation, and global adoption standards.

Cancer Vaccine Market: Growth Drivers & Challenges

Growth Drivers:

- Clinical Validation of mRNA–Checkpoint Inhibitor Combinations: The synergistic combination of mRNA-based personalized cancer vaccines with immune checkpoint inhibitors (ICIs) has emerged as the primary catalyst for market expansion. Mechanistically, cancer vaccines prime the immune system to recognize tumor-specific neoantigens, while ICIs (anti-PD-1/PD-L1 and anti-CTLA-4 antibodies) prevent T-cell exhaustion, creating a complementary therapeutic loop. This dual mechanism addresses a critical limitation of ICI monotherapy, which achieves response rates of only 15–30% in most solid tumors due to insufficient T-cell priming. The strategic shift in nomenclature from "cancer vaccine" to "individualized neoantigen therapy" reflects a deliberate industry adaptation to vaccine hesitancy concerns while maintaining scientific rigor.

- Expansion of mRNA-Based and Personalized Cancer Vaccine Platforms: Advancements in mRNA technology and personalized neoantigen vaccine development are significantly accelerating the cancer vaccine landscape by improving tumor-specific immune targeting. These platforms enable vaccines to be tailored to individual patients based on tumor mutation profiles, enhancing T-cell activation and immune memory against malignant cells. This mechanism increases treatment precision and reduces off-target toxicity compared to conventional oncology therapies, thereby improving clinical outcomes in solid tumors such as melanoma and colorectal cancer. The industry impact is reflected in rising clinical pipeline activity and stronger collaboration between pharmaceutical firms and immunotherapy developers.

Challenges:

- High Clinical Validation Complexity and Tumor Heterogeneity: The cancer vaccine market faces significant restraint due to the inherent biological complexity of tumors and the difficulty in achieving consistent clinical validation outcomes. The root cause lies in extreme tumor heterogeneity, rapid mutation rates, immune escape mechanisms, and highly variable antigen expression across patients, which makes it difficult to identify universally effective vaccine targets. In addition, the lack of standardized biomarkers and uncertainty in selecting appropriate clinical endpoints, such as immune response versus progression-free survival, further complicates trial design.

- Manufacturing and Scalability Constraints in Personalized Vaccine Production: A major restraint in the cancer vaccine market is the difficulty of scaling personalized vaccine manufacturing processes efficiently. The root cause is the individualized nature of many cancer vaccines, which require patient-specific tumor sequencing, neoantigen identification, and rapid GMP-grade production within tight timelines. This creates operational complexity across manufacturing, logistics, and quality control systems, particularly when maintaining strict cold chain requirements. The industry impact is reflected in production bottlenecks, limited batch scalability, and restricted throughput capacity, preventing widespread commercialization.

Cancer Vaccine Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

19.2% |

| Base Year Market Size (2025) |

USD 14.4 billion |

| Forecast Year Market Size (2035) |

USD 83.3 billion |

| Regional Scope |

|

Cancer Vaccine Market Segmentation Analysis:

Technology Segment Analysis

The molecular-based cancer vaccine segment is anticipated to garner the largest share of 92.6% in the cancer vaccine market by the end of 2035.

This reflects the technological maturation of gene-based platforms. Current demand drivers include the clinical validation of mRNA technology following COVID-19 vaccine deployment, which established manufacturing scalability and regulatory familiarity for oncology applications. The ability to encode multiple neoantigens within a single molecular construct addresses tumor heterogeneity, a critical limitation of cell-based alternatives. Industry adoption trends reveal a decisive shift toward nucleic acid platforms. The UK Vaccine Innovation Pathway reports 33 active cancer vaccine trials across 85 sites and 11 cancer types as of June 2025, with 1,937 patients recruited representing a 500% year-over-year increase in enrollment. Notably, 95% of tissue samples for molecular vaccine trials were processed within required timeframes, averaging 2.5 days from biopsy to preparation—demonstrating clinical feasibility of personalized molecular approaches.

Type Segment Analysis

The preventive sub-segment is projected to hold a considerable share of in the cancer vaccine market during the forecast period.

The sub-segment’s development is fueled due to its direct role in reducing the incidence of infection-driven cancers, particularly those linked to human papillomavirus (HPV) and hepatitis viruses. Current demand is driven by expanding national immunization programs, rising awareness of virus-associated cancer risks, and increased emphasis on early intervention strategies that reduce long-term oncology treatment burdens. Industry adoption trends show broader integration of HPV vaccines into adolescent vaccination schedules, including gender-neutral immunization policies across multiple countries, supported by school-based outreach programs.

Our in-depth analysis of the global cancer vaccine market includes the following segments:

|

Segment |

Sub-segment |

|

Technology |

|

|

Type |

|

|

Indication |

|

|

Distribution Channel |

|

Cancer Vaccine Market Regional Insights:

North America Market Trends & Insights:

North America maintains its leadership position in the global dental imaging market, capturing 36.7% of the market in 2035.

The United States is the primary contributor, driven by extensive R&D activity, high cancer burden, and strong integration of precision medicine in oncology care. Canada complements regional growth through government-supported cancer research initiatives and universal healthcare systems that facilitate access to innovative therapies. According to the U.S. Centers for Disease Control and Prevention (CDC), cancer remains one of the leading causes of death in the United States, underscoring the sustained demand for advanced prevention and treatment solutions, including cancer vaccines.

Canada serves as an important secondary market and clinical trial destination. The Canadian Agency for Drugs and Technologies in Health has developed early-stage health technology assessment frameworks specific to personalized cancer vaccines, providing reimbursement guidance that reduces market access uncertainty. Several U.S. developers have established Canadian trial sites to access the publicly funded healthcare system's centralized patient recruitment infrastructure.

Asia Pacific Market Trends & Insights:

The Asia Pacific is considered the fastest-growing region in the cancer vaccine market during the forecast timeline.

The market’s development in the region is supported by rising cancer incidence, improving healthcare infrastructure, and increasing government focus on immunization and precision medicine. Market demand is strengthening due to growing awareness of preventive oncology and expanding access to advanced biologics in urban healthcare systems. Industrial activity is accelerating as regional biotechnology hubs in China, Japan, and South Korea invest in immunotherapy research, vaccine manufacturing capacity, and clinical trial expansion. Governments across the region are actively supporting oncology innovation through national cancer control programs, funding for vaccine research, and public health initiatives aimed at strengthening early detection and prevention frameworks.

Japan maintains a distinct market position characterized by advanced sequencing infrastructure integrated within the national healthcare system and a regulatory environment that has granted early conditional approvals for innovative immunotherapy products. The Pharmaceuticals and Medical Devices Agency (PMDA) operates a dedicated consultation pathway for personalized cancer vaccines, providing regulatory guidance during preclinical and early clinical development—a framework that reduces development uncertainty.

China is a key growth engine in the region, driven by rapid expansion of its biotechnology sector, strong clinical trial activity, and government-backed innovation programs in precision medicine. Japan demonstrates strong adoption of advanced cancer therapies, supported by its aging population, high oncology treatment demand, and established regulatory pathways for regenerative medicine and immunotherapy.

Leading Companies Operating in the Global Cancer Vaccine Market:

The cancer vaccine market is characterized by a highly competitive and innovation-driven ecosystem dominated by global pharmaceutical companies and biotechnology firms focused on immuno-oncology, mRNA platforms, and personalized therapeutics. Leading players are actively investing in neoantigen-based vaccines, therapeutic cancer vaccines, and combination regimens with immune checkpoint inhibitors to enhance efficacy. Strategic collaborations between biotech innovators and large pharma companies are accelerating clinical development and commercialization.

Here is a list of key players operating in the global cancer vaccine market:

|

Company |

Specialty |

HQ |

Position |

|

Moderna |

mRNA-based cancer vaccines and immunotherapy platforms |

United States |

Leader |

|

BioNTech |

Personalized mRNA cancer immunotherapies |

Germany |

Leader |

|

Merck & Co. (MSD) |

Immuno-oncology and combination vaccine therapies |

United States |

Leader |

|

GSK |

Preventive and therapeutic vaccine development |

United Kingdom |

Major |

|

Roche |

Oncology biologics and immune-based cancer treatments |

Switzerland |

Major |

|

Bristol Myers Squibb |

Immune checkpoint and cancer immunotherapy integration |

United States |

Leader |

|

Pfizer |

Vaccine R&D and oncology pipeline expansion |

United States |

Major |

|

CureVac |

mRNA technology for cancer vaccine development |

Germany |

Niche |

Recent Developments

- In January 2026, Zydus Lifesciences Limited launched the world’s first biosimilar of Nivolumab in India under the brand name Tishtha™, reinforcing the company’s growing

- capability in advanced biologics and Immuno-Oncology.

- In June 2025, BioNTech SE and Bristol Myers Squibb entered into an agreement for the global co-development and co-commercialization of BioNTech’s investigational bispecific antibody BNT327 across numerous solid tumor types.

- In January 2025, Merck announced that the National Medical Products Administration (NMPA) of China approved GARDASIL® [Human Papillomavirus Quadrivalent (Types 6, 11, 16, and 18) Vaccine, Recombinant for use in males 9-26 years of age to help prevent certain HPV-related cancers and diseases.

Frequently Asked Question

In 2025, the cancer vaccine market exceeded USD 14.4 billion.

The cancer vaccine market is projected to reach USD 83.3 billion by the end of 2035, expanding at a CAGR of 19.2% over the forecast period (2026-2035).

The major players in the market are Moderna, BioNTech, Merck & Co., GSK, Roche, Bristol Myers Squibb, Pfizer, CureVac, and others.

In the Technology segment, the Molecular-based sub-segment is anticipated to capture the largest market share of 92.6% in the future and exhibit lucrative growth opportunities during 2026–2035. This growth trajectory is largely attributed to rising adoption of personalized mRNA-based immunotherapies and increasing integration of precision oncology approaches in cancer treatment.

North America is projected to hold the largest market share of 36.7% by the end of 2035 and provide more business opportunities in the future. Continuous investments in advanced immuno-oncology research, strong clinical trial infrastructure in the U.S., and supportive healthcare innovation ecosystems in Canada are fostering the region's dominance.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1015 |

Published Date: 16 Jun 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy