Report ID: 1005 |

Published Date: 27 May 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Antimony Market Outlook:

The global antimony market held a value of USD 2.6 billion in 2025 and is estimated to reach USD 4.9 billion by the end of 2035, expanding at a CAGR of 6.5% during the forecast period of 2026-2035. In 2026, the market is assessed at USD 2.6 billion.

The market is driven by its widespread applications across end use verticals, including chemicals and semiconductors. The rapid expansion of semiconductor manufacturing, electronics production, and advanced digital technologies is creating strong demand for antimony-based materials. Antimony is utilized in semiconductors, infrared detectors, diodes, and specialty electronic components due to its conductive and thermal properties. Increasing investments in artificial intelligence infrastructure, data centers, 5G deployment, and consumer electronics manufacturing are expected to support the long-term growth of the antimony market across technologically advanced economies.

Key Antimony Market Insights Summary:

Key Takeaways: Market Trends & Insights

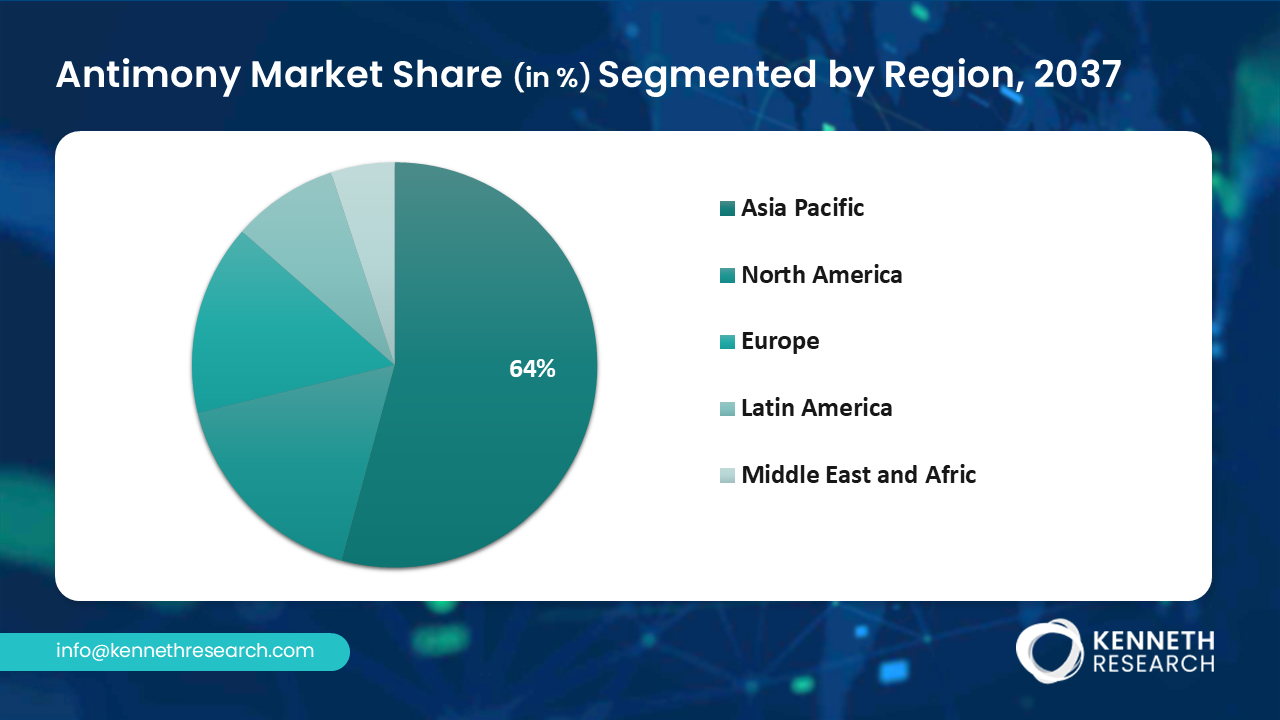

- Asia Pacific dominated the antimony market with a 64% share in 2025.

- In 2025, Europe contributed 18.1% of the overall antimony market share.

- The U.S. antimony market by application held a revenue share of 60% in 2025.

- By type, the trioxide segment is estimated to garner a share of 40% by the end of 2035.

- The major companies in the global antimony market are Albemarle Corporation, BASF SE, Dow, and Eastman Chemical Company, among others.

Market Drivers

- Rising Demand from Lead-Acid Battery Manufacturing

- Increasing Use in Flame Retardants

- Expansion of Semiconductor & Electronics Industries

- Growth in Renewable Energy & Energy Storage

Challenges

- Supply Chain Concentration in China Restricts Global Availability

- Declining Ore Grades Limit Sustainable Production

- Stringent Environmental Regulations Increase Compliance Costs

Antimony Market Overview & Supply Chain

Global investments in renewable energy generation and grid-scale energy storage systems are contributing significantly to antimony demand. Antimony-containing lead-acid batteries continue to play an important role in solar backup systems, off-grid power applications, and industrial energy storage infrastructure. Governments worldwide are increasingly investing in clean energy transitions and smart-grid modernization projects, which is expected to create sustained opportunities for antimony consumption in energy-related applications during the forecast period.

Commercially traded forms of antimony within the supply chain include ingots, granules, shots, powders, cast cakes, broken fragments, and single crystals. The metalloid occurs in the Earth’s crust at relatively low concentrations, estimated at approximately 0.2–0.5 parts per million. Due to its chalcophile nature, antimony is commonly associated with sulfur-bearing ores and is often recovered alongside heavy metals, including lead, silver, and copper. Although more than one hundred antimony-bearing minerals have been identified, stibnite (Sb₂S₃) remains the principal ore mineral used for antimony extraction.

Antimony Market Drivers & Challenge:

Growth Drivers:

- Rising demand from lead-acid battery manufacturing: The growing production and adoption of lead-acid batteries remains one of the primary drivers for the global antimony market. Antimony is extensively utilized as a hardening alloying element in lead-acid batteries to improve mechanical strength, corrosion resistance, and overall battery durability. These batteries continue to witness substantial demand across automotive starter batteries, industrial backup power systems, telecommunication infrastructure, renewable energy storage, and uninterrupted power supply (UPS) applications. Despite the rapid advancement of lithium-ion technologies, lead-acid batteries maintain a strong market presence due to their low cost, high recyclability, and reliable performance in heavy-duty and backup energy applications. In particular, increasing automobile production and the rising deployment of energy storage systems are accelerating the consumption of antimony-based battery alloys worldwide with sustainable measures. Government and industry statistics further validate this trend. According to the U.S. Environmental Protection Agency (EPA), nearly 99% of lead-acid batteries are recycled annually in the United States, making them one of the most recycled consumer products in the country. The EPA also highlighted that lead recovered from batteries accounted for approximately 1.7 million tons of recycled nonferrous metals in municipal solid waste streams, reflecting the large-scale circulation and continued utilization of lead-acid battery systems.

- Increasing use in flame retardants: The growing utilization of antimony compounds in flame-retardant applications is a major factor driving the expansion of the global antimony market. Among these compounds, antimony trioxide is the most widely consumed and is extensively used as a synergist in halogen-based flame-retardant formulations. It is commonly incorporated into plastics, textiles, electronics, construction materials, automotive interiors, insulation systems, and consumer appliances to reduce flammability and improve fire resistance. Rising urbanization, infrastructure development, and the growing production of electrical and electronic devices are further strengthening the demand for antimony-based flame-retardant solutions. In addition, industries such as automotive and aerospace are increasingly using flame-retardant polymers and composite materials to comply with stringent safety regulations and improve passenger protection. The increasing emphasis on fire safety standards across residential, commercial, and industrial sectors has accelerated the adoption of flame-retardant materials worldwide. Government-backed fire safety statistics also highlight the importance of flame-retardant technologies. According to the U.S. Fire Administration (USFA), local fire departments in the United States responded to an estimated 344,600 residential building fires in 2023, causing thousands of civilian injuries and billions of dollars in property damage annually.

Challenge

- Supply chain concentration in China restricts global availability: The global antimony market faces significant supply-chain challenges due to the high concentration of mining and refining activities in China. The country has maintained a dominant position in global antimony production for several decades, creating substantial dependency among downstream industries worldwide. Antimony is widely used in flame retardants, lead-acid batteries, semiconductors, military applications, and photovoltaic technologies, making uninterrupted supply critical for multiple industrial sectors. However, the heavy reliance on China has increased concerns regarding raw material availability, export restrictions, geopolitical tensions, and pricing volatility. In recent years, tightening environmental regulations, declining ore grades, and production controls within China have further constrained global supply. These developments have intensified efforts among countries such as the United States, Australia, and Canada to diversify sourcing and strengthen domestic critical mineral strategies.

Antimony Market Size and Forecast:

| Report Attribute | Details |

|---|---|

| Base Year |

2025 |

| Forecast Year |

2026-2035 |

| CAGR |

6.5% |

| Base Year Market Size (2025) |

USD 2.6 billion |

| Forecast Year Market Size (2035) |

USD 4.9 billion |

| Regional Scope |

|

Antimony Market Segmentation Analysis:

Type Segment Analysis

The trioxide segment is projected to account for a revenue share of 40% by the end of 2035. The growth of this segment is being strongly supported by increasingly stringent fire safety and regulatory standards across industries such as construction, automotive, electrical and electronics, textiles, and consumer products. Rising demand for flame-resistant materials in infrastructure projects and electronic equipment manufacturing continues to strengthen consumption of antimony trioxide globally.

From a supply-chain standpoint, production of antimony trioxide remains highly concentrated in China, which controls a substantial portion of the world’s antimony mining, smelting, and refining operations. Recent regulatory tightening, environmental inspections, and export control measures implemented by Chinese authorities have created procurement challenges and elevated pricing pressures across major importing regions, including Europe, North America, and Japan. Despite ongoing cost fluctuations and supply-chain disruptions, market demand has remained resilient due to the essential role of antimony trioxide in fire protection applications and industrial manufacturing processes.

Over the coming years, the segment is anticipated to maintain its strategic importance, driven by sustained growth in flame-retardant systems, electronics production, urban infrastructure expansion, and industrial safety requirements. Nevertheless, the industry is expected to continue facing challenges associated with supply security, environmental sustainability regulations, raw material concentration risks, and volatility in global antimony pricing.

End use Segment Analysis

The flame retardant application segment is projected to account for a considerable share of market revenue throughout the forecast period. In the United States, flame-retardant applications represented a significant share of total antimony consumption in 2024, highlighting their dominant role in downstream demand. Moreover, one of the major global uses of bromine involves the production of brominated flame retardants (BFRs), which are commonly formulated using antimony oxide compounds, along with applications in clear brine drilling fluids. U.S. apparent bromine consumption in 2024 also increased compared to the previous year, reflecting growing industrial utilization. The strong demand for flame-retardant materials across construction, electronics, automotive, and industrial sectors has significantly contributed to the expansion of flame-retardant manufacturing activities and associated processing equipment industries.

Our comprehensive analysis of the antimony market covers the following key segments:

|

Segment |

Sub-segment |

|

Type |

|

|

Product |

|

|

Production Method |

|

|

End use |

|

Antimony Market Regional Analysis:

Asia Pacific Market Insights

Asia Pacific antimony market is anticipated to garner the largest revenue share of over 64% during the assessment period. This growth is supported by the strong manufacturing and supply capabilities of countries such as China, Japan, and India, particularly in products including automotive components, coatings, and pigments. Japan remains an important participant in the global pigments industry, contributing approximately USD 244 million to pigment and titanium dioxide exports in 2023. Antimony is most commonly extracted from the sulfide ore mineral stibnite (Sb₂S₃), although it is also found in metallic and complex sulfosalt mineral forms across the Asia-Pacific region, including cylindrite, boulangerite, jamesonite, tetrahedrite, and pyrargyrite. In terms of global reserves, China maintained the leading position in 2023 with approximately 640 kilotons of antimony reserves, followed by Russia with around 350 kilotons and Kyrgyzstan with nearly 260 kilotons.

India antimony market is witnessing steady growth due to rising demand from flame retardants, lead-acid batteries, electronics, and automotive applications. Increasing industrialization and infrastructure development are supporting the consumption of antimony trioxide in plastics, textiles, and construction materials. The country remains largely import-dependent for antimony supply, with China being a major sourcing partner. Expanding electronics manufacturing and government-led industrial initiatives are expected to further strengthen market demand during the forecast period.

China antimony sector dominates the overall market owing to its substantial mining reserves, refining capacity, and export presence. The country plays a critical role in supplying antimony for flame retardants, batteries, semiconductors, and military-grade applications worldwide. Strong domestic demand from electronics, renewable energy, and industrial manufacturing sectors continues to support market expansion. However, stricter environmental regulations, export controls, and resource management policies in recent years have contributed to global supply-chain volatility and rising antimony prices.

North America Market Insights

The North America antimony market is driven by growing demand from flame retardants, lead-acid batteries, defense equipment, and semiconductor applications. Increasing investments in critical mineral supply-chain security and domestic resource development are supporting regional market growth. The region remains heavily dependent on imports, particularly from China, creating concerns regarding supply stability and pricing volatility. Rising adoption of renewable energy storage systems and stricter industrial safety regulations are expected to further boost antimony consumption.

The U.S. antimony market is expanding due to increasing demand across defense, energy storage, electronics, and flame-retardant industries. The country relies significantly on imported antimony because of limited domestic mining and refining capacity. Government initiatives aimed at strengthening critical mineral independence and reducing reliance on foreign supply chains are encouraging investments in recycling and domestic resource development. Growing demand for lead-acid batteries, military applications, and industrial safety materials continues to support market expansion.

Antimony market in Canada is supported by rising interest in critical mineral exploration and strategic resource development. The country possesses antimony-bearing mineral deposits that are gaining attention amid global supply-chain diversification efforts. Increasing demand from flame-retardant materials, battery technologies, and industrial alloys is contributing to market growth. Government support for mining investments, clean energy initiatives, and domestic critical mineral supply chains is expected to create long-term opportunities for antimony production and processing activities in Canada.

Competitive Landscape: Antimony Market

Here is a list of key players operating in the global antimony market:

- Albemarle Corporation (The U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- BASF SE (Germany)

- Dow (The U.S.)

- Eastman Chemical Company (The U.S.)

- Huntsman Corporation (The U.S.)

- LANXESS AG (Germany)

- ICL Group Ltd. (Israel)

- Clariant AG (Switzerland)

- Italmatch Chemicals S.p.A. (Italy)

- Nabaltec AG (Germany)

- J.M. Huber Corporation (The U.S.)

- FRX Innovations (Canada)

- DuPont (The U.S.)

- DSM (Netherlands)

- THOR Group (UK)

- Alexium International (Australia)

- Jiangsu Jacques Technology Co., Ltd. (China)

- Rin Kagaku Kogyo Co., Ltd. (Japan)

- Sanwa Chemical Co., Ltd. (Japan)

- TOR Minerals International Inc. (The U.S.)

Recent Developments

- In February 2026, Nyrstar announced the first shipment of commercially produced antimony metal from its Port Pirie multi-metals facility in Australia. This marked a major milestone in Australia’s efforts to establish an independent mine-to-metal supply chain for critical minerals. The antimony produced at the demonstration plant will initially be supplied to an Australian domestic manufacturer, while future shipments are expected to serve customers across Europe, Asia, and the United States. The project was accelerated with financial support from the Australian and South Australian governments and is intended to reduce global dependence on concentrated antimony supply sources. Nyrstar also stated that the Port Pirie facility has the long-term potential to produce up to 5,000 tonnes of antimony annually, supporting industries such as semiconductors, defense, automotive, and energy storage.

- In November 2025, Nyrstar, a subsidiary of Trafigura, commenced pilot-scale antimony metal production at its Port Pirie facility in South Australia. The project was supported through a joint investment package from the Australian and South Australian governments aimed at strengthening Western critical mineral supply chains. The facility is expected to scale up antimony production for semiconductor, defense, and electronics applications.

- In September 2025, United States Antimony Corporation (USAC) announced that it secured a five-year contract worth up to USD 245 million from the U.S. Defense Logistics Agency to supply antimony metal ingots for the U.S. national defense stockpile. The agreement highlights increasing government focus on strengthening domestic critical mineral supply chains and reducing dependence on Chinese imports for defense-related applications

Frequently Asked Question

The global Antimony Market was valued at USD 2.6 billion in 2025 and is projected to reach USD 4.9 billion by the end of 2035, expanding at a CAGR of 6.5% during the forecast period of 2026–2035.

Major growth drivers of the antimony market include increasing demand from lead-acid battery manufacturing, rising usage of antimony trioxide in flame-retardant applications, expansion of semiconductor and electronics industries, and growing deployment of renewable energy and energy storage infrastructure globally.

The trioxide segment is anticipated to account for nearly 40% of the global antimony market share by the end of 2035 due to its extensive utilization in flame-retardant formulations across construction, electronics, automotive, and textile industries.

The flame retardants segment is projected to dominate the global antimony market throughout the forecast period owing to increasing fire safety regulations and growing demand for flame-resistant materials in electrical, construction, automotive, and industrial applications.

Asia Pacific is expected to dominate the global antimony market during the forecast period, supported by strong mining reserves, refining capabilities, and industrial demand from countries such as China, India, and Japan.

Major companies operating in the global antimony market include Albemarle Corporation, BASF SE, Dow, Eastman Chemical Company, Huntsman Corporation, and LANXESS AG among others.

Why Choose Kenneth Research ?

-

Insight with Impact : We don’t just gather data — we uncover stories, trends, and opportunities that fuel business growth.

-

Experts Who Get It : Our team speaks your industry’s language and knows what really matters to your customers and market.

-

Custom-Built for You : Forget one-size-fits-all. We craft research and consulting solutions as unique as your business vision.

-

Partners, Not Just Providers : We work with you, not for you — collaborating closely to turn insights into smart, strategic moves.

-

Results That Speak : Our work powers brands, startups, and industry leaders alike — with a track record of ideas that work in the real world.

Report ID: 1005 |

Published Date: 27 May 2026 |

Report Format: |

Delivery Timeline: 48-72 Business Hours

Copyright © 2025 Kenneth Research. All rights reserved. Terms of Use | Privacy Policy